China’s rise as the world’s dominant light vehicle (LV) exporter is no longer a trend, it is a structural shift that is fundamentally reshaping the global Vehicle Carrier market. In just five years, Chinese full-year LV exports have grown from 1.6 million units in 2021 to a projected 10 million in 2026 across all transport modalities, with 4.06 million units already exported in January–May alone, representing 63% year-on-year growth according to CAAM. The scale of this transformation is remarkable, but what makes it even more compelling is the resilience behind it.

Ongoing tensions in the Middle East threatened approximately 15% of China’s LV export volumes and around 10% of global Vehicle Carrier demand. Rather than slowing down, Chinese OEMs have responded by rapidly redirecting volumes to alternative markets, adeptly navigating both geopolitical disruptions and trade barriers. Brazil has emerged as one of the fastest-growing destinations during January-May 2026, up 235% year-on-year, while the UK, Belgium, and Italy each posted triple-digit growth driven by surging EV demand.

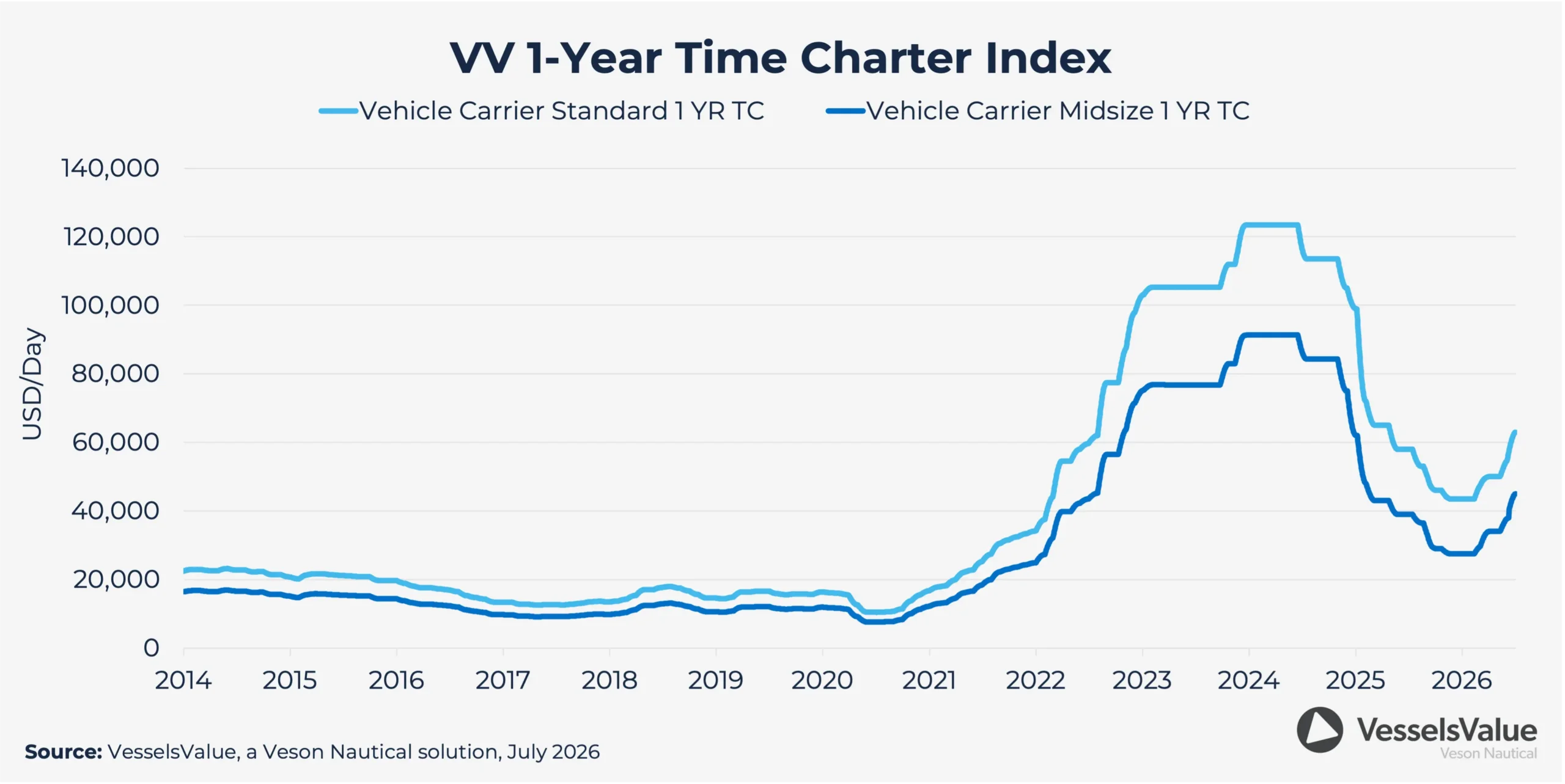

How charter rates are responding to the tight supply-demand balance

The consequences for the Vehicle Carrier market have been profound. Global fleet capacity expanded by 3.3% in the first half of 2026, yet global car-mile demand grew at exactly the same pace, keeping the market in a persistently tight supply-demand balance. Charter rates have responded accordingly, with VesselsValue’s One-Year 6,500 CEU Time Charter Index rising c.45% since the start of the year and now sitting at 67,000 USD/day.

The market’s strength is further evidenced by recent charter activity: EPS owned Lake Rotorua (7,060 CEU, Apr 2026, Jinling Shipyard Nanjing) was fixed to SAIC Anji Logistics in May at an incredible high price 90,000 USD/day representing a 70% premium above the One-Year 6,500 CEU Index, while SFL Conductor (6,500 CEU, Nov 2006, Shin Kurushima Onishi) and SFL Composer (6,500 CEU, Aug 2005, Minami Nippon) were both fixed to COSCO Shipping Lines at 40,000 USD/day for 34 months, a clear sign that operators are increasingly willing to commit to longer-term charters to secure tonnage.

Learn more about Vehicle Carriers in the Shipping Market Outlook: Q3 2026

Why Container vessels are absorbing the export overflow

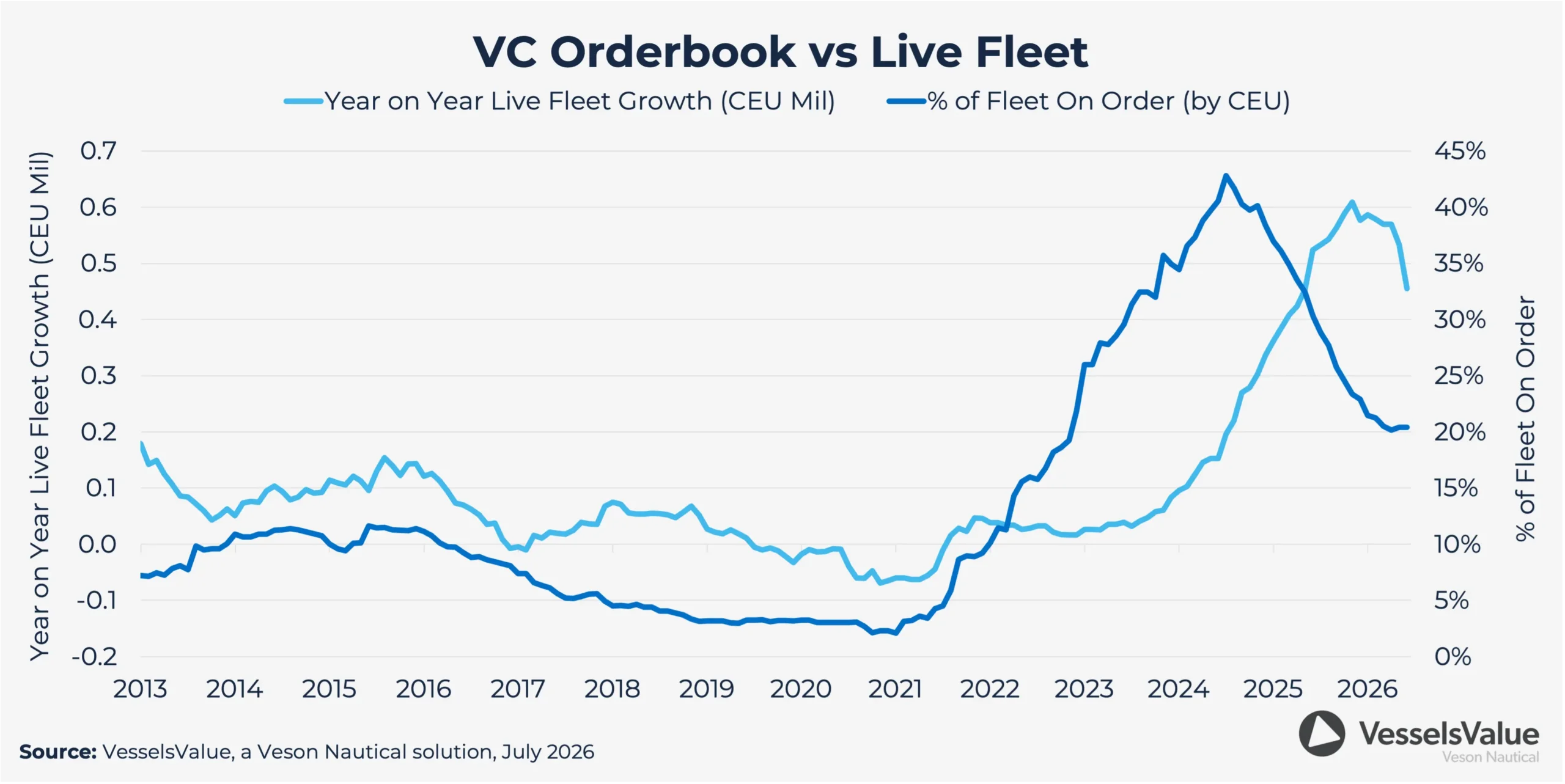

The most striking consequence of China’s export ambitions, however, is the growing use of container vessels as an overflow solution. With LV exports targeting 10 million units across all transport modalities this year and fleet supply expected to grow only 7.6% year-over-year, not all of which will be available for full-year utilisation given delivery timing, VC capacity simply cannot accommodate the full volume of exports out of Asia.

Last year we estimated over one million cars were exported via alternative shipping modalities, primarily containers; this year, driven by an increasingly unbalanced market, we estimate that figure could reach around two million units — a record high. This is no longer a temporary workaround; it is a structural feature of the trade and a clear signal of a market operating beyond its limits.

How shipowners are racing to build capacity

Shipowners have taken notice. Newbuilding activity rebounded sharply in the first half of 2026, with 29 confirmed Vehicle Carrier orders placed against just two in the same period of 2025, a 1,350% year-over-year increase.

Among the most significant commitments was the return of Global Car Carriers (GCC), the recently rebranded MSC-owned company, which ordered four dual-fuel LNG 8,600 CEU units, the largest vessels by capacity ever placed by a tonnage provider, plus four additional dual-fuel LNG 7,000 CEU units, with the stated ambition to double its fleet.

Asset values have followed the same trajectory, with 10-year values for standard 6,500 CEU and 4,000 CEU vessels up approximately 10.5% from the start of the year.

China’s vehicle export machine is running at full speed, and the global Vehicle Carrier market is being reshaped around it. The question is no longer how much China can export, it is whether the industry can build ships fast enough to keep up.

Explore the trends behind this shift in the 2026 Mid-Year Shipping Market Report and get a first look at Vehicle Carriers in the Q3 Shipping Market Outlook, which examines what’s next for rates, newbuilds, and values.