The first half of 2026 was defined by the closure of the Strait of Hormuz following US-Israeli military operations against Iran in late February. The disruption rippled across shipping markets: asset values recovered strongly across most segments, ordering activity rebounded across several sectors, and Chinese shipyards further consolidated their dominance.

Our 2026 Mid-Year Shipping Market Report covers all 10 market sectors in depth, with newbuilding, S&P, and demolition data across every sector, plus headline transactions and country-by-country breakdowns.

Here’s a quick look at how each market moved in 1H 2026:

Bulkers

Secondhand Dry Bulk values rose across every sector and age group in 1H 2026, with mid-aged Supramax and Handysize tonnage posting some of the strongest gains. VLCC newbuilding orders climbed to 229 vessels, driven by a c.650% year-on-year jump in Greek ordering.

In the report, Senior Content Analyst Rebecca Galanopoulos examines Greece’s dramatic return to the market more closely.

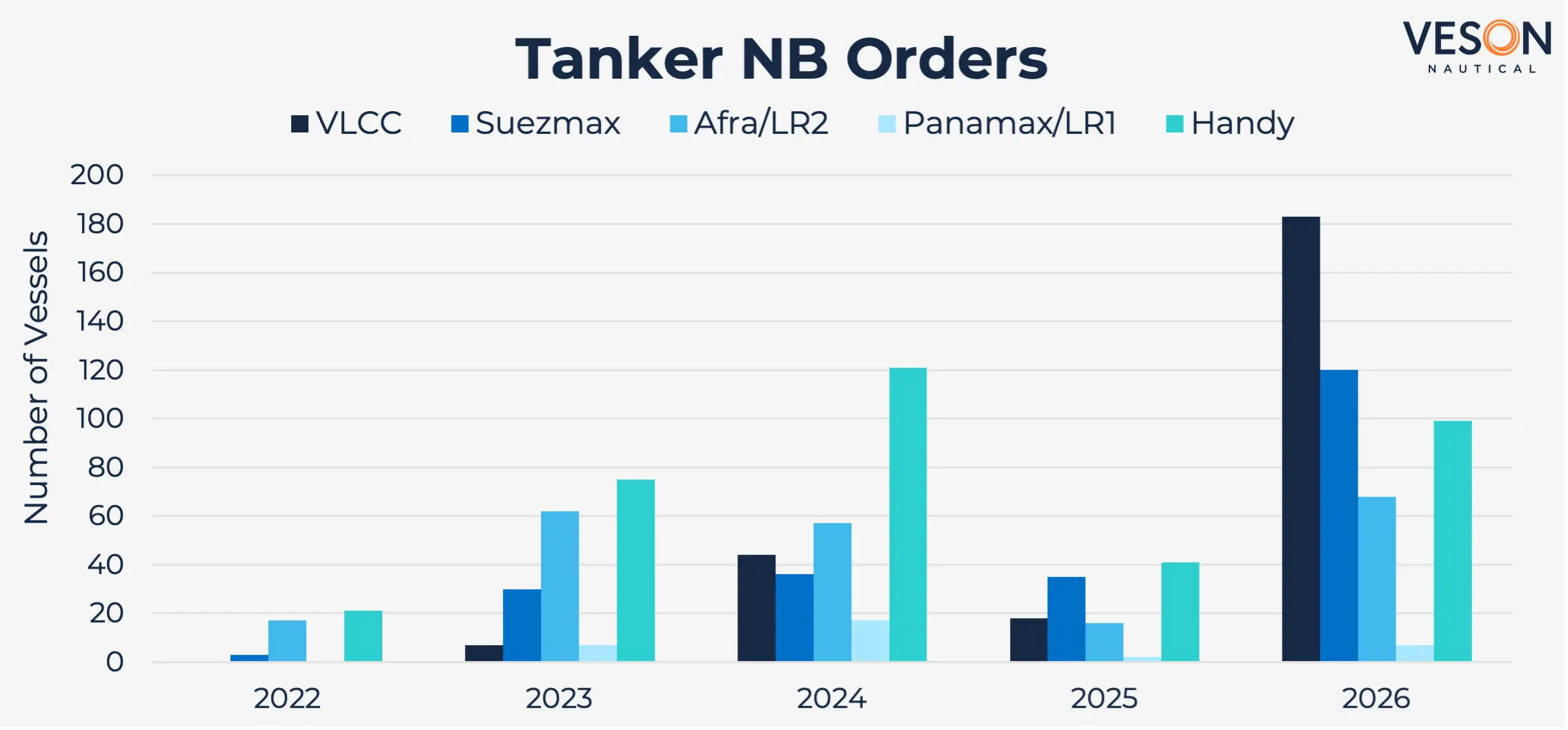

Tankers

VLCC one-year time charter rates ran c.136% above where they were this time last year, pushing Crude Oil Tanker values toward levels last seen during the 2008 super cycle. Newbuilding orders surged to 183 vessels, up from just 18 in 1H 2025. Galanopoulos breaks down what’s driving the rush back into VLCC ordering in the full report.

Containers

Container charter rates and asset values held stable in 1H 2026, up c.9% on average year-on-year even as the Red Sea remained closed to traffic. S&P activity, however, fell to its lowest first-half level in recent years.

LPG

VLGC spot rates surged 150% in 1H 2026 after roughly 30% of global LPG export volumes were cut off by the Hormuz closure. Yet S&P transaction volumes fell even as values climbed, an unusual disconnect that Maritime Analyst Jarl Milford unpacks in the full report.

LNG

Spot charter rates for two-stroke LNG vessels swung between USD 30,000/day and USD 250,000/day in 1H 2026. Newbuilding activity rose 150% year-on-year, led by orders in the Large LNG segment.

Get the full breakdown in the 2026 Mid-Year Shipping Market Report

Offshore

AHTS values firmed across every size and age band in 1H 2026. Newbuilding orders, meanwhile, fell c.74% year-on-year. In the report, Maritime Analyst Peter Edwards examines why owners have held back on new investment.

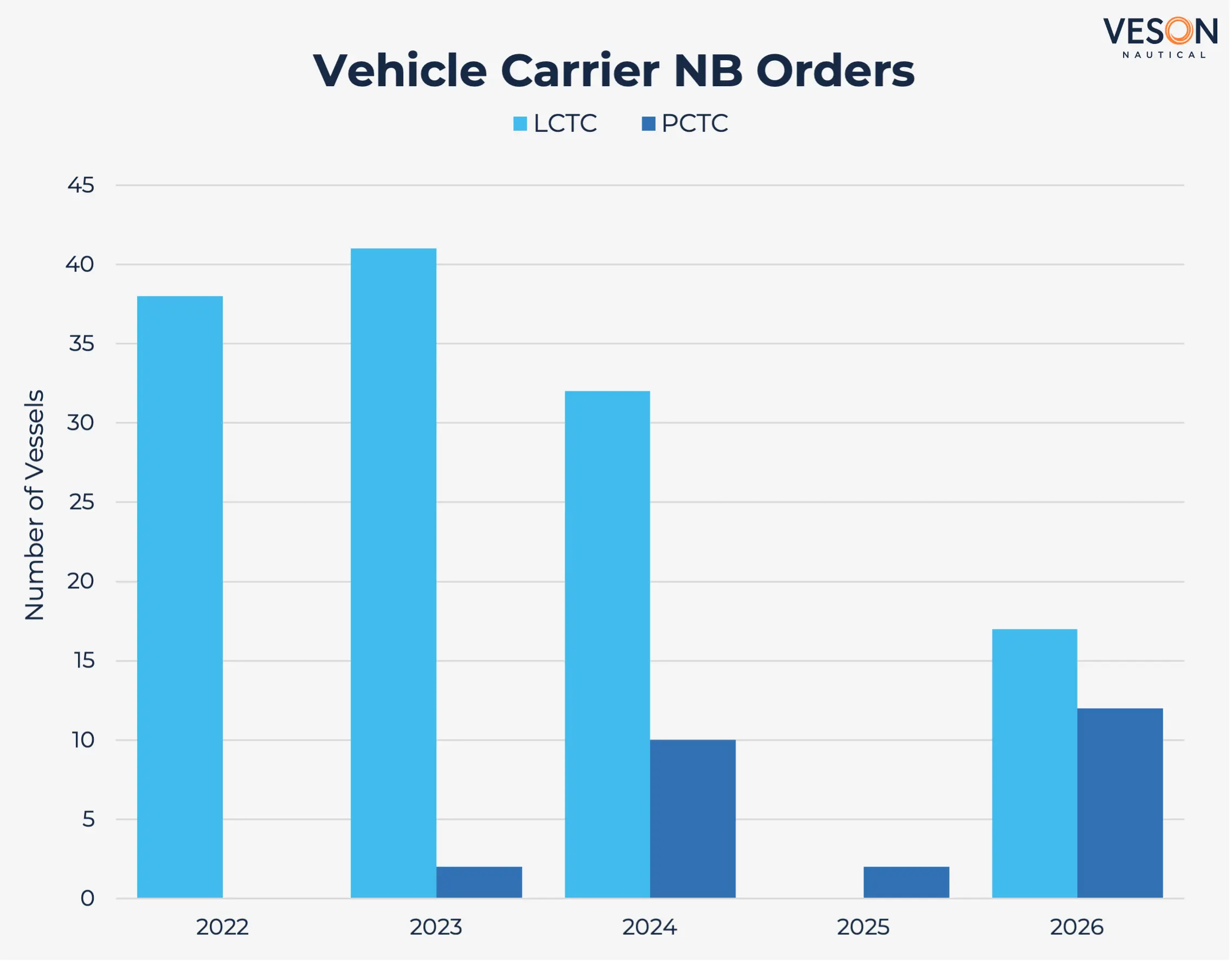

Vehicle Carriers

China exported 4.06 million light vehicles between January and May, up 63% year-on-year. Newbuilding orders rebounded 1,350% year-on-year, though, as Maritime Analyst Andrea De Luca examines in the full report, a meaningful share of Chinese exports are still moving on Container ships instead.

RORO

The shortsea RORO market performed broadly in line with the previous year in 1H 2026. S&P activity was down c.46% year-on-year, as owner-operators found little reason to deploy fresh capital.

Ferry

The European Ferry sector gathered momentum in 1H 2026. Demolition activity fell 82% year-on-year, among the lowest levels in the five-year dataset.

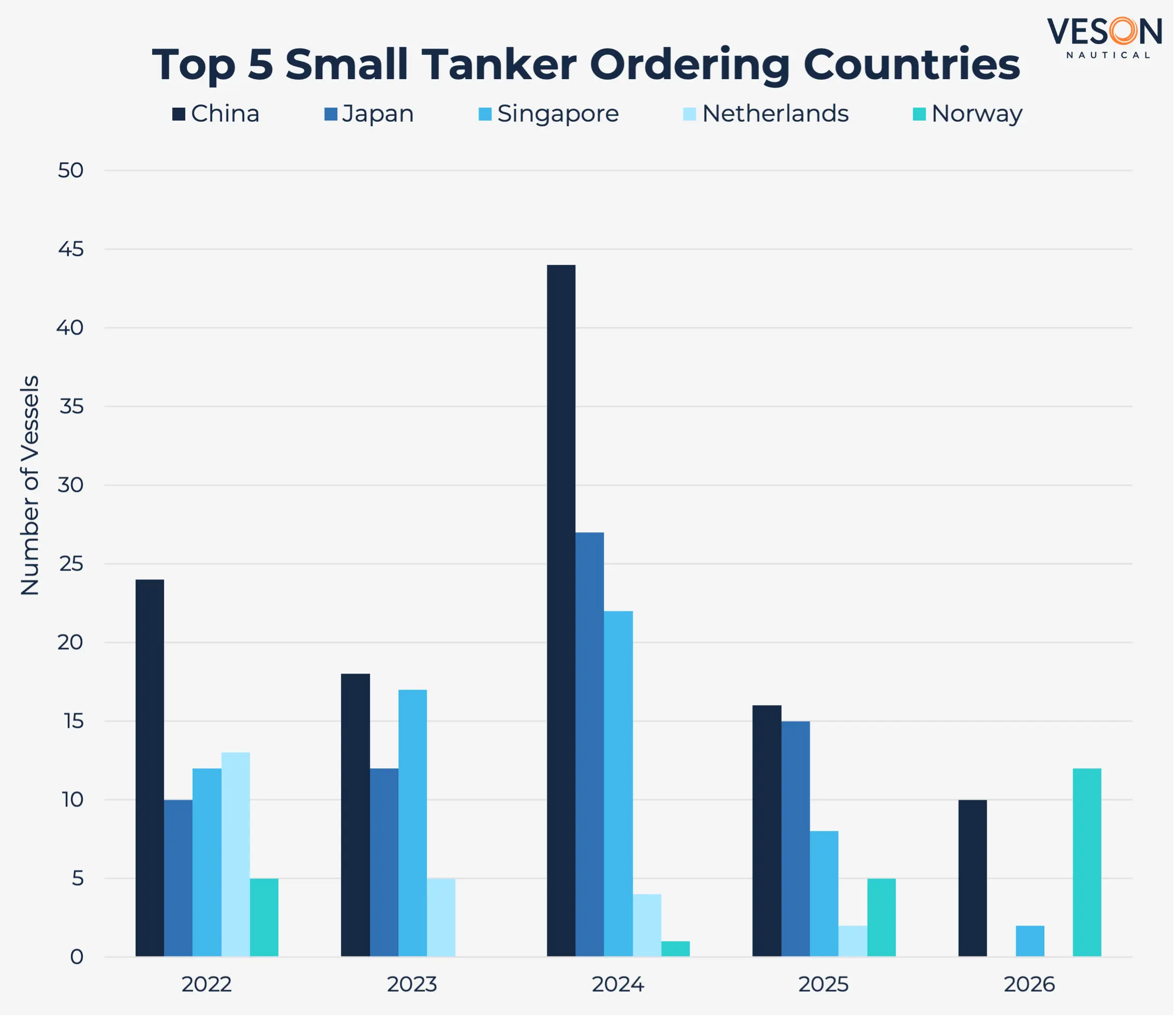

Small Tankers

Long-haul Chemical Tanker rates firmed considerably in 1H 2026 as Norway emerged as the most active ordering nation, surpassing China for the first time in the five-year dataset. Senior Maritime Analyst Charlie Litterick dives deeper into the market in the full report.

This is just a glimpse of what is all included in the 2026 Mid-Year Shipping Market Report. Across 60+ pages, the report includes newbuilding, S&P, and demolition data for each of these sectors.

All information provided is for informational purposes only. To the extent that any provided information is based on Veson Data, Veson excludes to the extent permitted by law all implied warranties relating to fitness for a particular purpose, including any implied warranty that Veson Data is accurate, complete, or error free. Veson Data are collated and processed by and on behalf of Veson in accordance with methodologies and assumptions published and updated by Veson from time to time which do not take into account particular circumstances applicable to individuals and therefore; (i) are made available on an ‘as is’ basis; (ii) are not intended as a substitute for formal valuations; (iii) should not be used solely as trading, investment, or other advice; and (iv) are not intended as a substitute for professional judgement. To the extent permitted by applicable law, Veson shall have no liability to party for any errors or omissions in the content of the information provided.