As we enter the third month of escalating conflict in Yemen, this has prompted significant rerouting of vessels with far-reaching consequences for global trade and transport. The latest trade data from Veson Nautical indicates a notable shift in traffic patterns. Geopolitical tensions and conflict have raised maritime security concerns in the region, given its strategic importance and critical maritime trade routes. In addition, the ongoing crisis in Yemen has implications for traffic through the Suez Canal and therefore Egypt, which may incur substantial costs due to the disruptions in trade and transport. However, this situation could potentially serve as a catalyst for increased diplomatic efforts to broker peace, considering the economic losses incurred by the Egyptian government as a result of the crisis. Understanding the economic impact on Egypt and specifically the Suez Canal might encourage a more proactive approach towards resolving the conflict and mitigating its adverse effects on global trade.

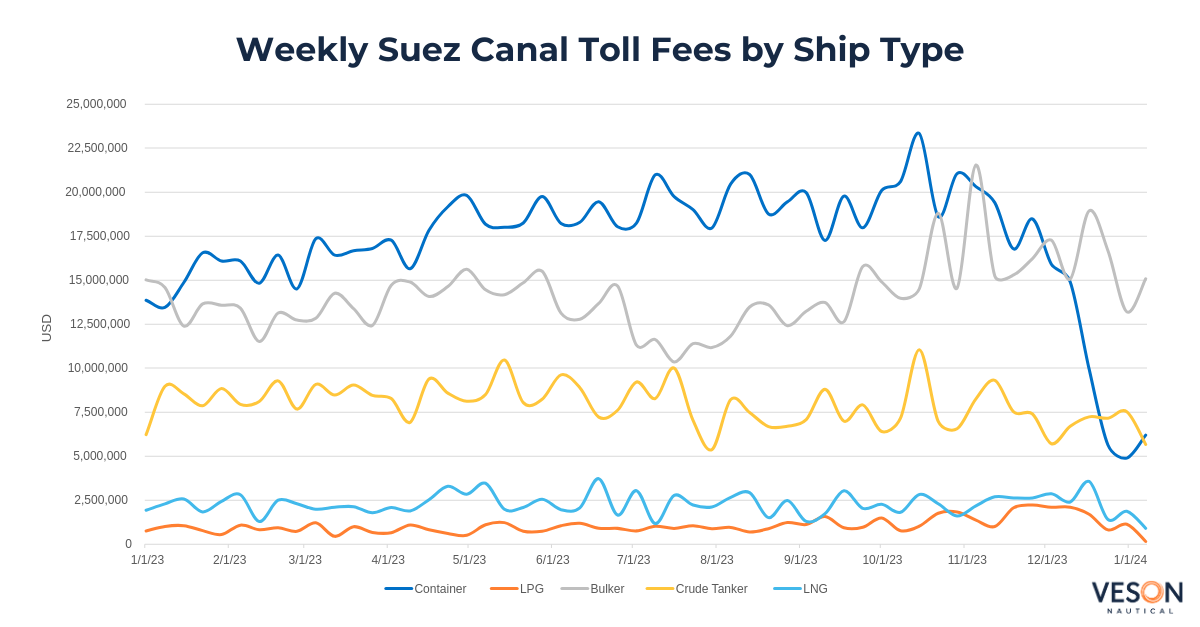

We take a look at the changes in the Suez Canal toll fees for crude Tankers, Bulkers, LNG, LPG and Containers from the beginning of 2023 to early January 2024. This analysis provides valuable insight into the financial implications for the Suez Canal and for the Egyptian government as Suez Canal transits reach a low.

Overall toll fees fall c.40% since November 2023

Looking at the weekly toll fees graph*, overall tolls have fallen by c.40% since the end of November from USD 47 mil to USD 28 mil. Container tolls have significantly decreased, falling by c. 66% from the end of November, where estimated fees fell from c. USD 18 mil that week to USD 6 mil at the start of January. However, in percentage terms the LPG sector experienced the biggest drop with tolls down by c.93% from USD 1 mil at the end of November to USD 153,000 in the first week of January. LNG tolls ranked third, with a fall of c.66% followed by Crude Tankers which experienced a fall of c.23% from USD 7.3 mil to USD 5.7mil in January. Bulkers were the least affected, with a comparatively modest decline of about 7%.

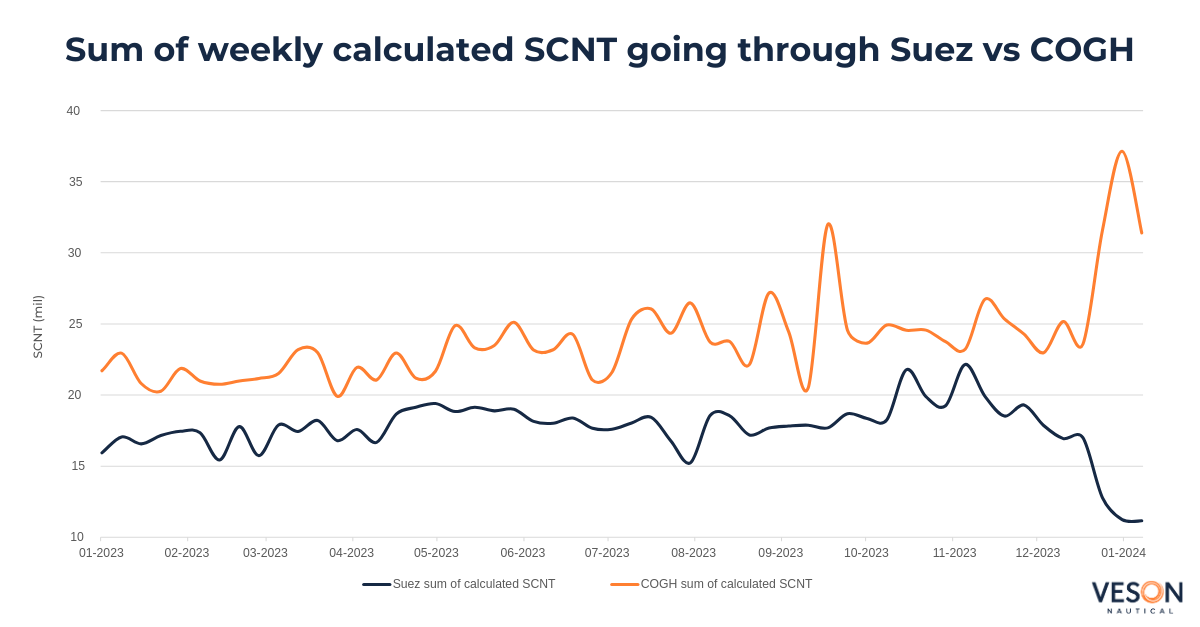

The analysis of the sum of weekly calculated SCNT (Suez Canal Net Tonnage) transiting through the Suez Canal versus the Cape of Good Hope (graph 2) reveals a noteworthy trend. The graph illustrates a reduction in SCNT through the Suez Canal and a corresponding increase in the Cape of Good Hope region/transit zone, which is particularly evident since November 2023. Month on month, there has been a significant decline of approximately 38% in the sum of weekly calculated SCNT through the Suez Canal, while the sum of SCNT going around the Cape of Good Hope has increased by about 25%.

This shift is attributed to a surge in attacks targeting vessels in the region, compelling ship operators to alter their routes. The consequences of these alterations include increased costs (including rising oil prices), shipment delays, threats to maritime security and concerns about geopolitical instability. Without resolution to the situation, this could further impact trade flows and increase commodity prices and emissions.

As vessels divert away from the affected area and opt for the Cape of Good Hope route, tonne-mile demand for various sectors has increased, providing support to vessel earnings.

In addition, the intervention of the US and UK military with strikes has caused a spike in oil prices. While levels have not risen as dramatically as they did following the invasion of Ukraine, there are ongoing threats of retaliation from Iranian-backed forces, suggesting potential further disruptions to oil supply in the future.

Mixed impact on cargo markets

The situation’s influence on various cargo markets has been mixed. In the crude Tanker sector, rates for Suezmaxes and Aframaxes have firmed since the start of December, up by around 16% and 63% respectively. The route around the Cape of Good Hope more than doubles the length of voyages from the Middle East to Europe and therefore reduces the supply of available tonnage in the market.

In the Container sector, the diversion has reversed a steady downward trend in freight rates since 2022. A large number of vessels have diverted from the Red Sea to travel around the Cape of Good Hope, and this has also led to increasing earnings with Post Panamax period rates for one-year up by c.7% from December.

Although the impact on the Bulker sector is significantly lower than for other markets despite the usual dip in earnings during January, rates have remained historically high for this time of the year, even after a decrease from the peak in December.

Conclusion

The complex interconnection of geopolitical events, maritime security concerns and global trade dynamics underscores the multifaceted challenges facing the shipping industry in the current scenario. Although longer transit times and increased earnings may be acceptable in the short term, looking further ahead, they could be outweighed by increased costs to the owner.

From the perspective of Egypt, reduced traffic through the Suez Canal and therefore a lower income from toll fees is likely to persist for the foreseeable future. However, understanding the economic repercussions on the nation could foster a more proactive approach to resolving the conflict and alleviate its adverse effects on global trade.

Interested in how real-time market data from Veson Nautical can help you make more confident and informed decisions? Explore our data and analytics solutions, and learn more about VesselsValue and Oceanbolt today.

*Estimated toll fees were calculated using the toll fees pre-15th Jan.