From surging VLCC values to record orderbook activity, Greek owners are driving both sides of the market. As Posidonia 2026 approaches, we examine the key trends shaping the Tanker S&P and newbuilding markets in 2026 using VesselsValue data.

10 year-old VLCC values reach historic highs

At USD 117.33 mil, 10-year-old VLCCs are trading at historically elevated levels, nearly 2.5 times the long-run median of USD 48.68 mil, levels not seen since the 2008 supercycle.

The surge has been driven by a confluence of factors: aggressive acquisition campaigns from buyers such as Sinokor tightening available supply, Strait of Hormuz disruption bolstering ton-mile demand, strong freight earnings keeping older tonnage commercially viable, and sustained demand for aged vessels in sanctions-adjacent trades.

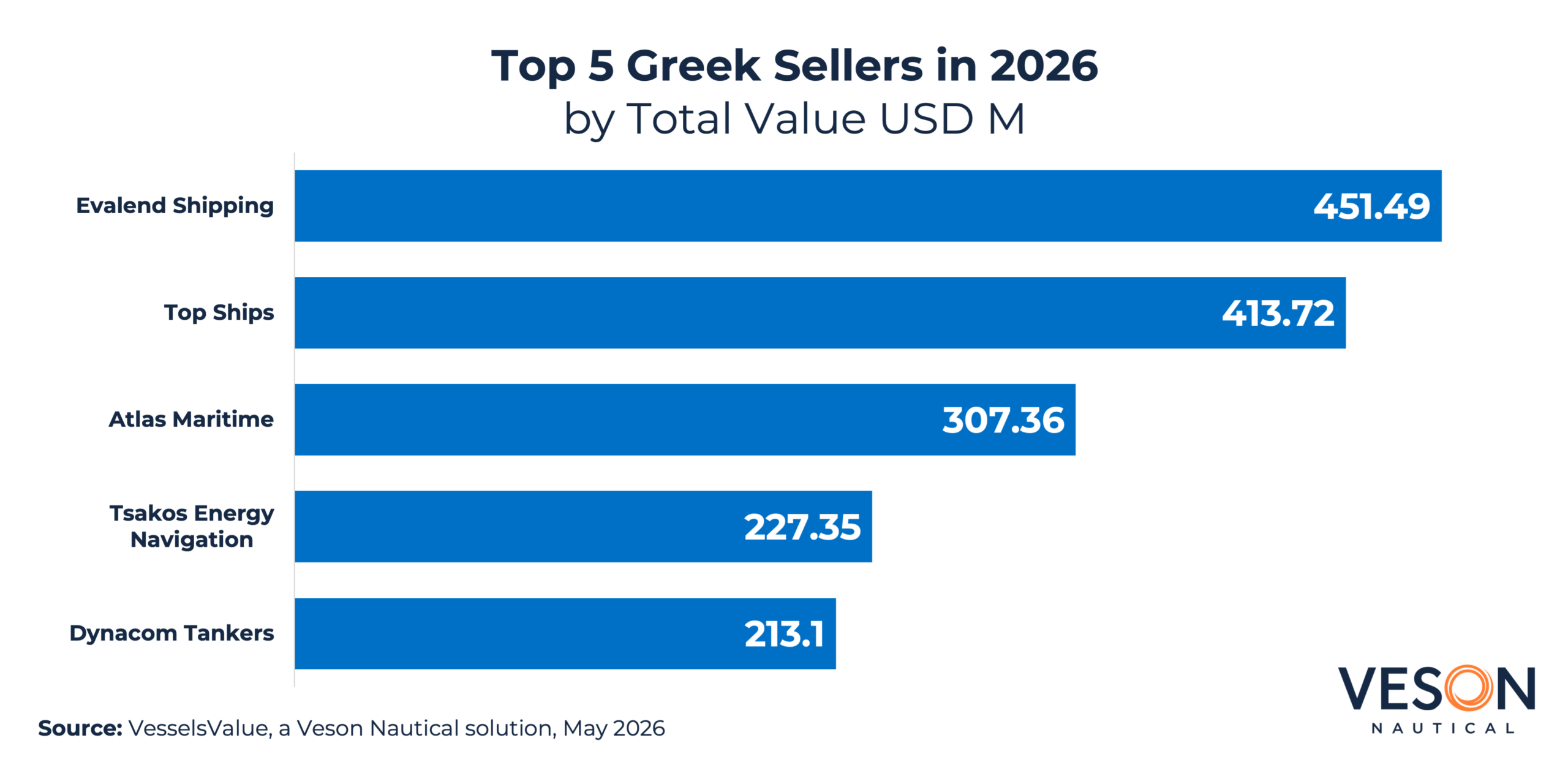

Greece’s top sellers capitalise on elevated values

Greek owners have been active sellers in 2026, with the top five alone accounting for USD 1.61 bil in combined vessel sales. Since the beginning of the year, values for 15-year-old VLCCs have risen +35.19% to USD 80.53 mil, rewarding sellers willing to move older tonnage.

Evalend Shipping leads the pack at USD 451.49 mil, followed by Top Ships at USD 413.72 mil. Atlas Maritime and Tsakos Energy Navigation followed at USD 307.36 mil and USD 227.35 mil respectively, while Dynacom Tankers completed the top five at USD 213.1 mil, a notable entry given their typically low sale activity, driven by opportunistic disposals to Sinokor Merchant Marine, who paid competitive above-market prices for VLCC tonnage at the time.

How Greece’s top buyers are reinvesting

On the buying side, the top five Greek operators acquired just over USD 1 bil in tonnage in 2026, led by Minerva Marine at USD 312.17 mil. Minerva’s acquisitions reflected a preference for modern, high-specification tonnage, including two newbuild Suezmax tankers from Samsung HI at USD 120.00 mil apiece and a 2018-built Aframax from COSCO Zhoushan at USD 71.00 mil.

Thenamaris and Okeanis Eco Tankers followed at USD 235.19 mil and USD 194.73 mil respectively, while Spring Marine Management and Silk Searoad Maritime completed the top five at USD 150.25 mil and USD 132.77 mil, reflecting continued appetite for tonnage among major Greek operators.

The contrast between Greece’s top sellers and buyers tells a clear story of fleet renewal in 2026; owners such as Evalend Shipping have moved quickly to monetise older tonnage at historically strong values, while buyers like Minerva Marine have reinvested in modern, high-specification vessels, pointing to a broader repositioning dynamic across the Greek owner base.

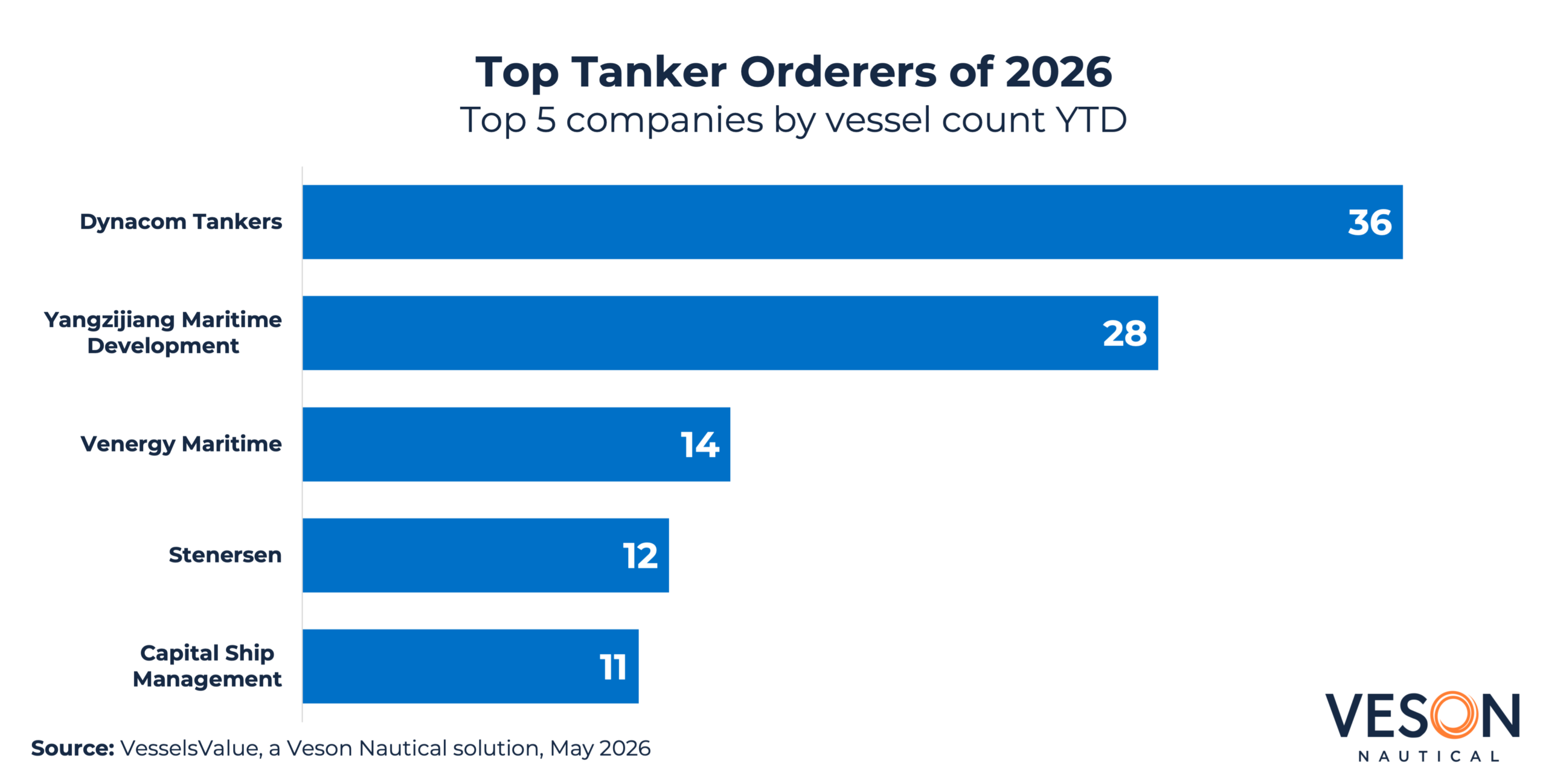

Greece drives global newbuilding activity

The top five Tanker orderers have collectively placed 101 newbuilding orders in 2026, with Dynacom Tankers leading at 36. Yangzijiang Maritime Development and Venergy Maritime followed with 28 and 14 orders respectively, while Stenersen and Capital Ship Management completed the top five with 12 and 11 orders.

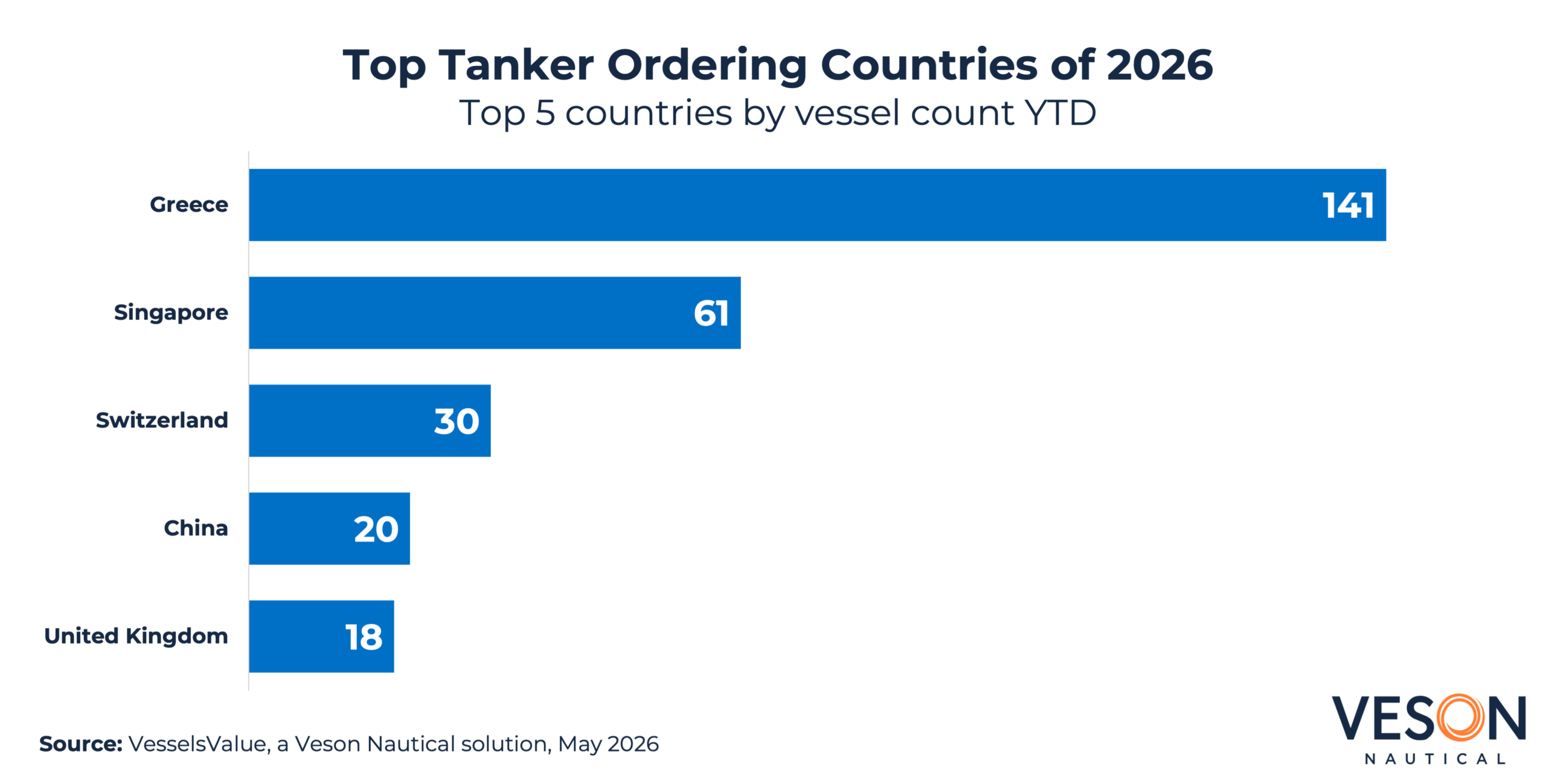

Greece placed 141 orders, accounting for over a third of the 351 total Tanker orders recorded this year to date, which represents a near fourfold increase on the 86 orders placed over the same period last year. The number of Tankers on order now represent over 20% of the total fleet, a significant increase compared to three months ago with only 15% of the fleet on order.

Greece’s ordering appetite is more than double Singapore’s 61 vessel orders, reinforcing the picture of Greek operators aggressively reinvesting in new tonnage while simultaneously monetising older vessels at historically elevated values.

Switzerland and China followed with 30 and 20 orders respectively, while the UK rounded out the top five with 18 orders.

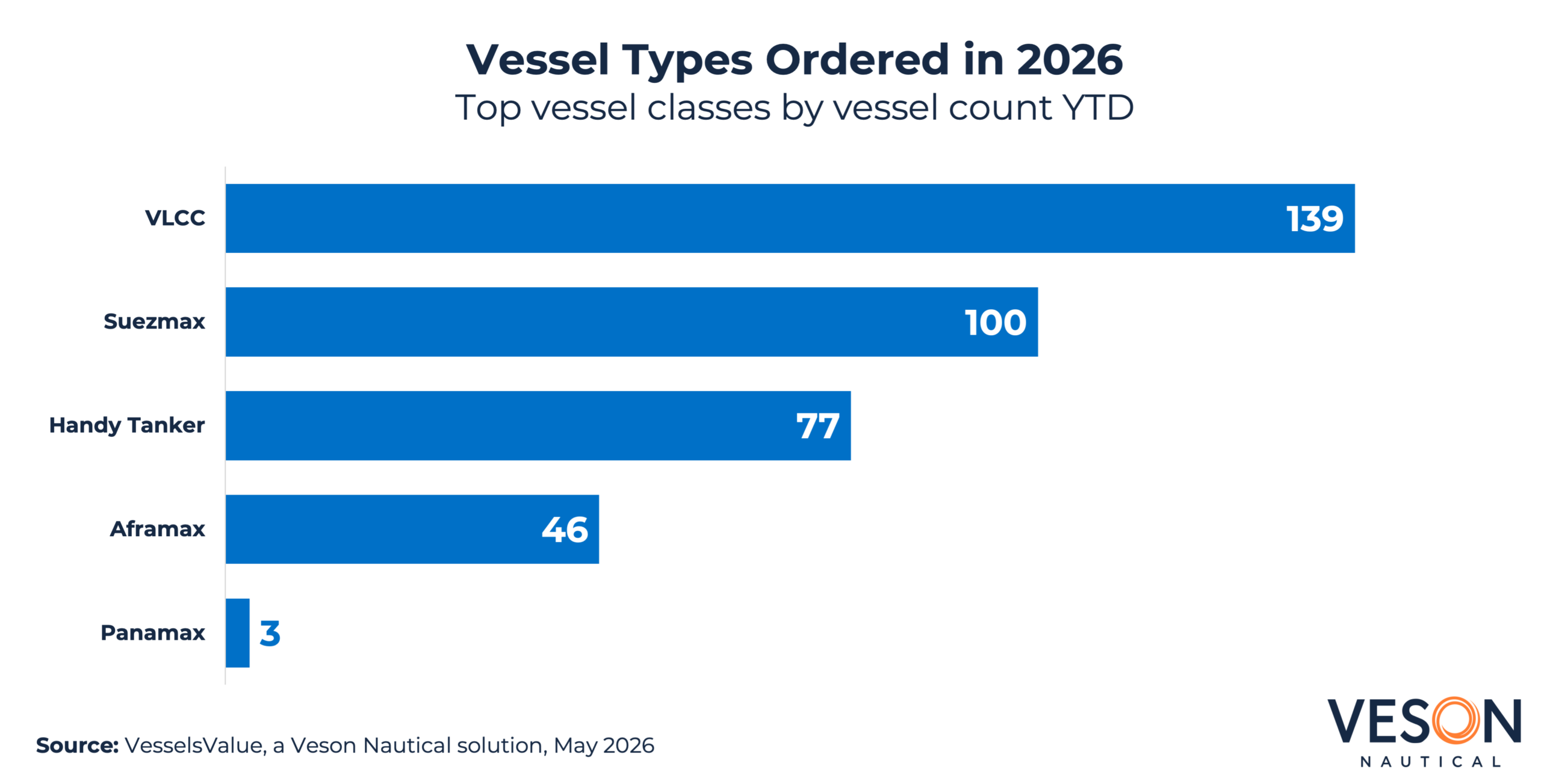

VLCC orders dominate the 2026 Tanker orderbook with 139 units placed, more than any other vessel type, reflecting the strong asset values and ton-mile demand that have characterised the sector this year.

VLCC secondhand sales have surged in parallel; 96 vessels have changed hands this year to date compared to just 52 over the same period last year, with Sinokor accounting for the majority of purchasing activity. Suezmax and Handy Tanker orders followed at 100 and 77 respectively, while Aframax accounted for 46 orders. Panamax recorded the fewest at just 3, suggesting limited appetite for mid-range tonnage amid the current market dynamics.

Together, the data paints a vivid picture of a Tanker market in transition. Greek owners are capitalising on historically elevated asset values to offload aged tonnage while simultaneously placing newbuilding orders at a record pace. Much of this activity has been supported by VLCC demand, in large part by Sinokor’s aggressive acquisition campaign, and the ongoing Strait of Hormuz disruption.

With ordering volumes running nearly four times ahead of the same period last year, 2026 is shaping up to be a landmark year for Tanker S&P and newbuilding markets.