Last week’s framework deal between the US and Iran marked the biggest turning point for the VLCC market since the closure of the Strait of Hormuz in late February.

Under the 14-point MOU, Iran will gradually reopen the Strait of Hormuz, the US will lift its naval blockade of Iranian ports as well as remove sanctions on the country, and Iran will be permitted to freely sell its oil. Reopening the strait would unlock the roughly 214 Tankers backed up in the Gulf as of late last week, though numbers remain approximate due to spoofing and vessels going dark.

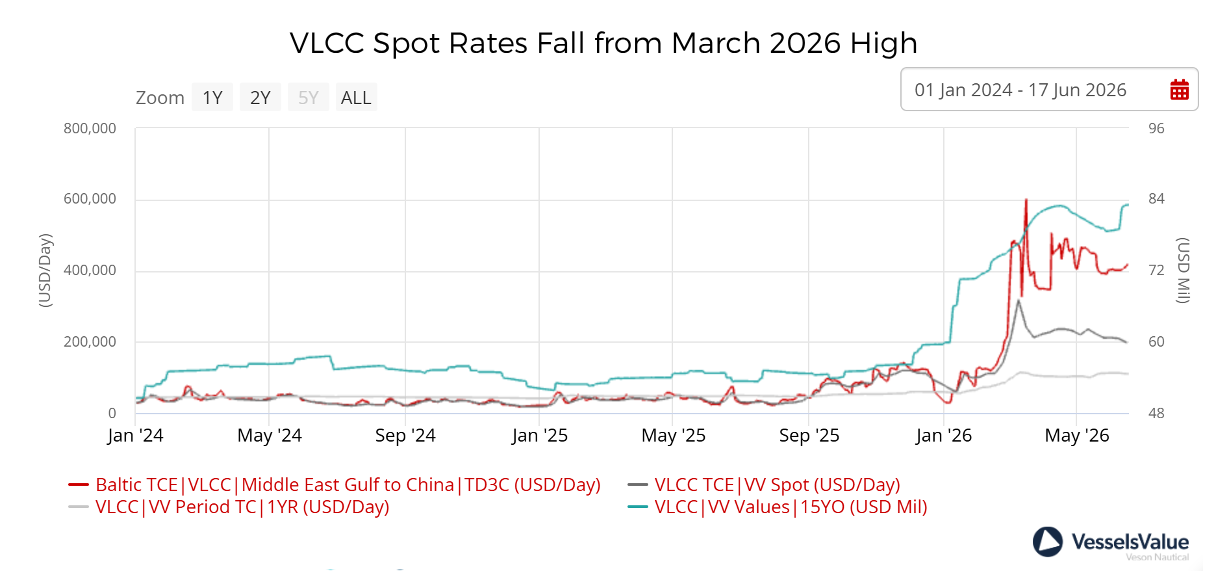

Spot rates have already pulled back from the March all-time high of around 318,400 USD/day to around 196,800 USD/day, a decrease of c.38%. The market has likely not yet found a floor, as it remains to be seen if and by how much further rates will fall should the reopening fully materialise. The market nevertheless remains cautious: the 60-day ceasefire extension is a temporary agreement rather than a permanent resolution, and with the deal now signed, the focus shifts to underwriters, as insurance markets must now respond to a completed agreement rather than a tentative one.

As of June 19, just 16 vessels had left the Inner Persian Gulf and are mainly from regional owners, with the majority of owners and operators awaiting clarity on insurance coverage before committing tonnage to the route.

This week, the IMO released a formal evacuation plan for the hundreds of vessels and roughly 11,000 seafarers still stranded in the Persian Gulf, with traffic through the Strait of Hormuz picking up but remaining below pre-war levels. The US-Iran MOU permits toll-free passage for 60 days, though Iran has signalled it may seek to charge vessels beyond that window, leaving full normalisation uncertain.

Weekly dirty tanker flow data underlines the scale of the disruption to date. China, the primary destination for Middle East VLCC cargoes, is importing below its 52-week average, while US dirty tanker exports have reached near parity with Saudi Arabia at 4.93 mil MT and 4.91 mil MT respectively, reflecting the trade flow rerouting that has partially offset the loss of Gulf volumes.

The market direction is clear: the closure has meaningfully compressed the world’s most important crude trade lane. A sustained reopening would likely see Chinese import volumes recover quickly, and with them, VLCC demand.

This freight market strength has been a significant driver of asset value appreciation and transaction activity. Second-hand VLCC sales have increased by c.49% year-on-year, with 113 sales reported thus far in 2026, compared to 76 over the same period in 2025.

Newbuilding orders have seen an even more dramatic surge, up c.917% to 183 so far in 2026 against just 18 over the same period last year, a clear signal that owners are positioning for a prolonged period of elevated earnings. Resale values for -1 year old 320,000 DWT VLCCs reflect this sentiment, rising 17.46% since the start of the year from 136.77 USD mil to 175.12 USD mil, with the highest recorded sale reaching 163 USD mil. For context, the market value of a vessel at the point of ordering was 123.99 USD mil, meaning sellers are locking in close to 40 USD mil in profit.

More broadly, VLCC values across the board have soared to 18-year highs in 2026. Values for 15-year-old 310,000 DWT VLCCs, for example, have risen c.38.75% year to date from 59.87 USD mil to 83.07 USD mil. With rates now softening on deal optimism, the near-term trajectory for asset values will depend heavily on whether the Hormuz reopening holds.

REPORT