Shipping markets closed 2025 with mixed performance across vessel classes, shaped by geopolitical disruptions, evolving trade patterns, and more selective investment. Routing shifts around the Cape of Good Hope continued to influence demand, while regulatory and financing pressures affected earnings and ordering decisions.

Veson’s free, 60+ page 2025 End-of-Year Shipping Market Report provides a detailed view of these developments and how they are shaping early expectations for 2026.

Here is a brief overview of how the major market sectors performed:

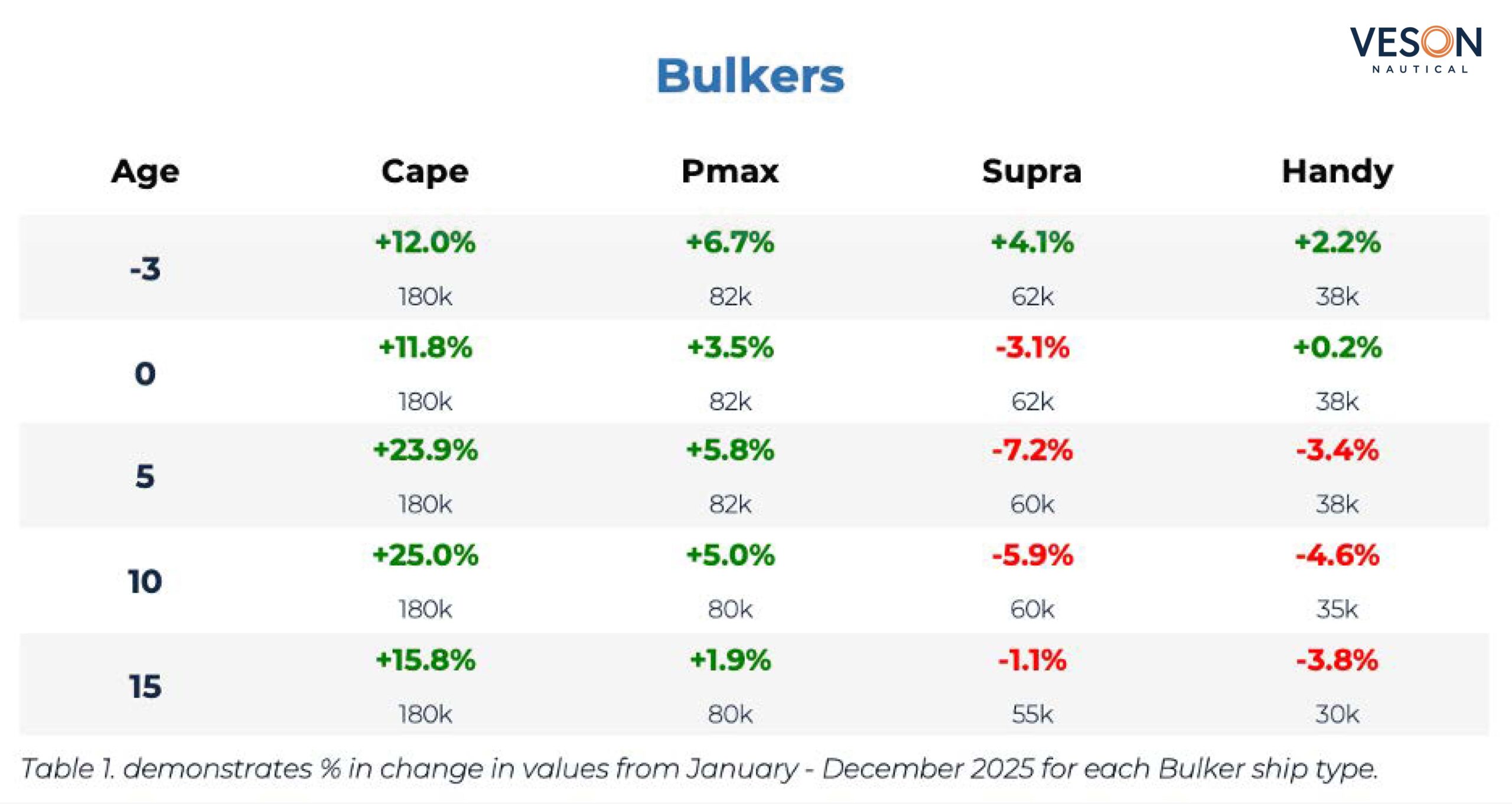

Bulkers

Capesize values were a key source of strength, with five-year-old units up c.23% YoY and 10-year-old units up c.25%, supported by extended voyage distances driven by Red Sea diversions.

Newbuilding activity picked up meaningfully in the second half of the year, rising from 169 orders in 1H to 227 in 2H, yet the full-year total of 396 contracts still marked the lowest level since 2019 — reflecting owner caution amid high prices, long delivery timelines, and uncertainty around future fuel technologies.

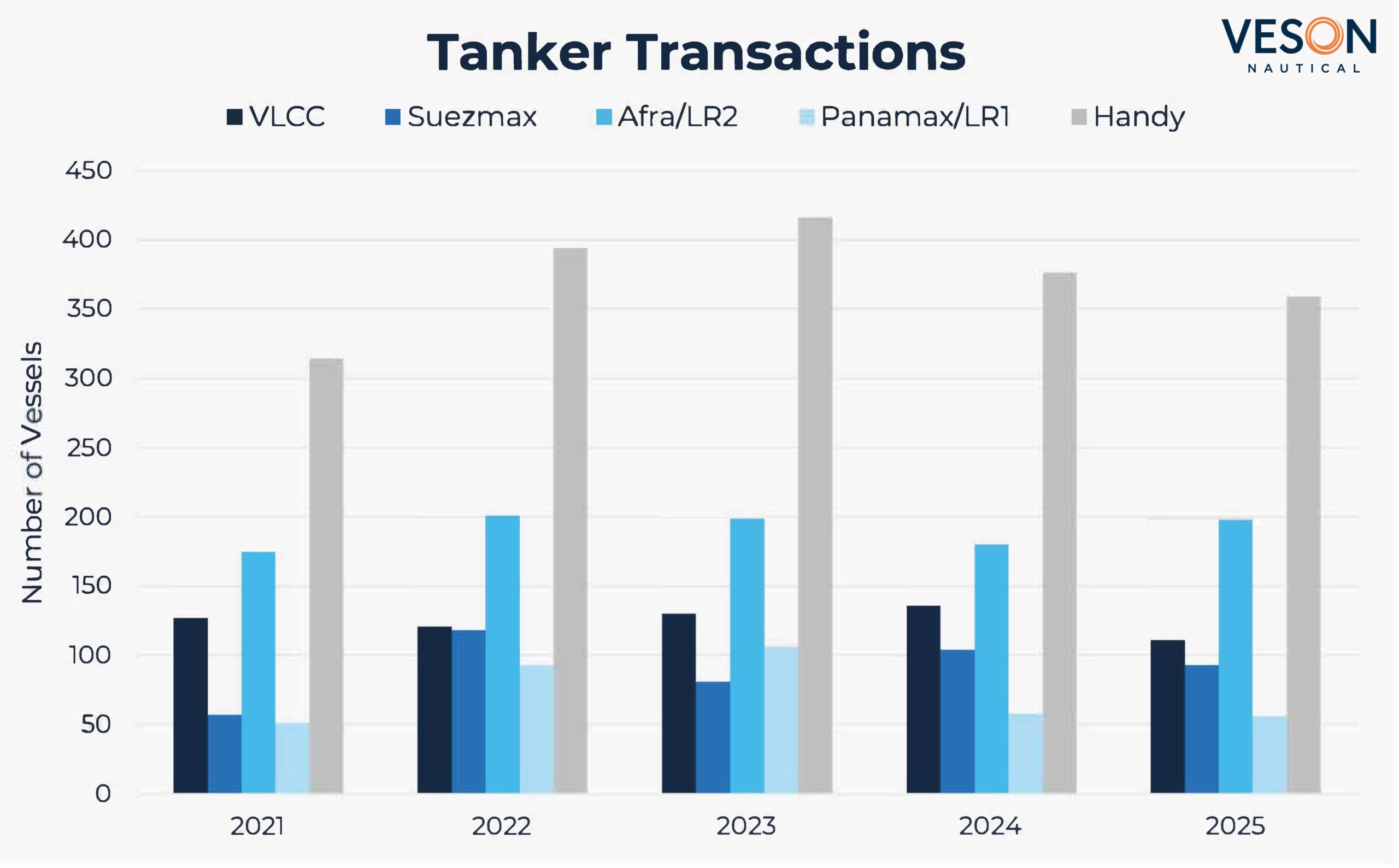

Tankers

Crude Tanker values appreciated across most age categories, while product Tankers faced declines, underscoring a widening split between the two markets. Newbuilding orders contracted sharply to 291 vessels (-43% YoY), as owners balanced long-term fleet renewal needs against limited yard capacity and delivery delays.

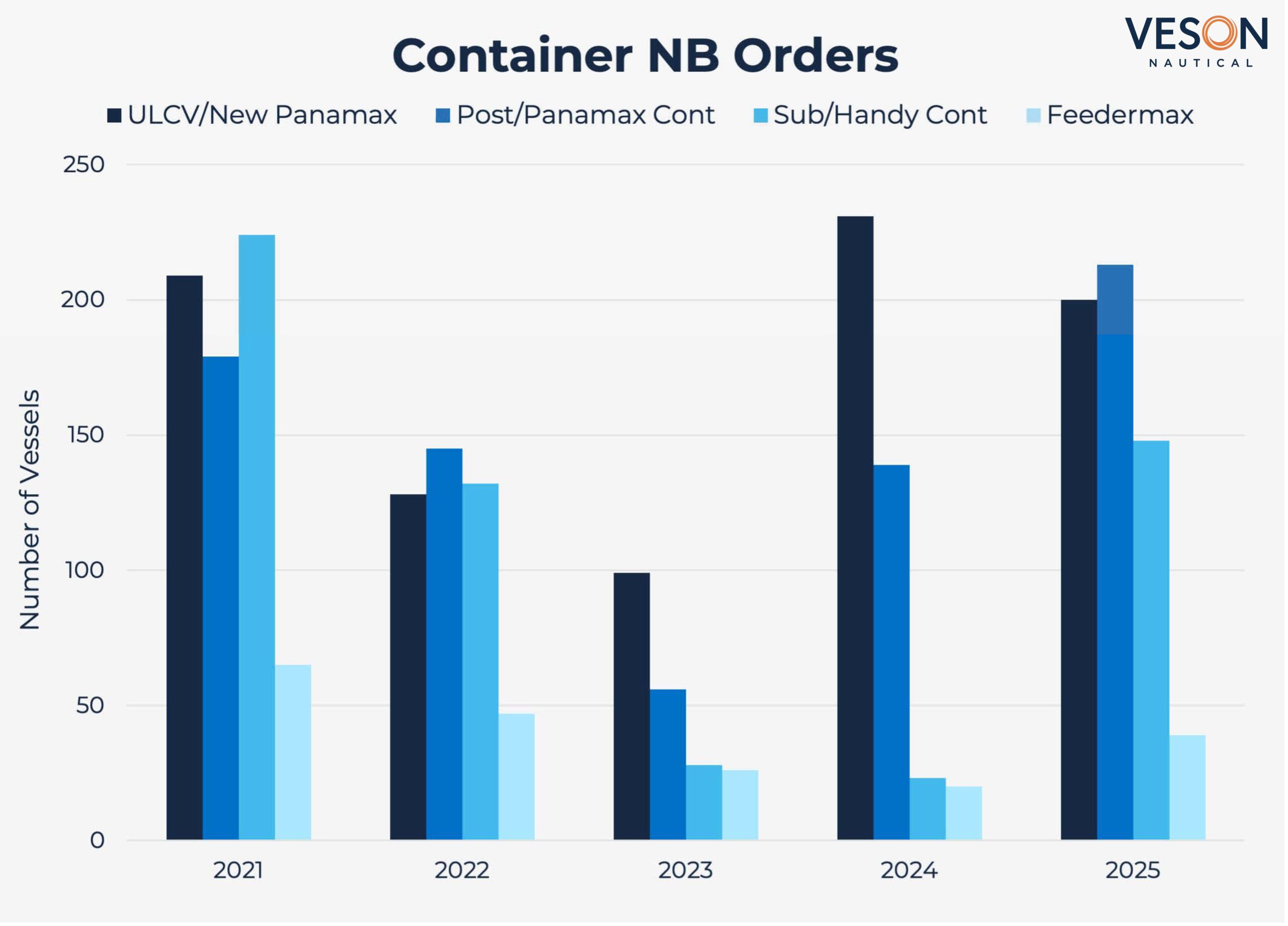

Containers

Demand for mid-size secondhand tonnage remained strong, with 15YO Handy rising c.22% and Panamax vessels rising c.14% in value over the year as charter markets stayed firm. Newbuilding surged to 600 orders (+42% YoY), but scrapping remained minimal at 13 vessels, underscoring tight supply and extended vessel lifecycles.

LPG

VLGC earnings averaged USD 49,300/day, up 14% from 2024, supporting firmer values at the large end. At the same time, ordering activity fell to 44 vessels (-70% YoY), and S&P volumes dropped 44%, reflecting more measured investment after two years of elevated activity.

LNG

Muted earnings shaped the LNG market in 2025, with one-year TC rates for large vessels down 60% from 2024 and asset values declining across all age groups. Newbuilding activity also eased, with 35 large LNG orders placed (-48% YoY), while demolition rose to 14 vessels as older steam turbine units faced increasing operational pressure.

Vehicle Carriers

A substantial wave of new deliveries expanded fleet capacity by 10.8% YoY, contributing to a correction in the VV 1-Year 6,500 CEU Index to USD 43,500/day (-56% YTD). Although asset values softened (down c.43% for 15YO units), S&P activity remained limited at 25 deals, consistent with tight availability of quality tonnage.

Offshore

PSV utilization softened by c.2.5% through the year to c.77%, while AHTS/AHT utilization held steady near 82%, reflecting a more measured pace of activity compared with 2023–24. Despite this cooler backdrop, values for modern PSV and AHTS tonnage continued to firm, and owners placed 37 new orders as early fleet renewal discussions began to take shape.

Download the full report for deeper analysis of values, newbuilding activity, S&P trends, and demolition across Bulkers, Tankers, LPG, LNG, Containers, Vehicle Carriers, Offshore, RoRo, Ferry, and Small Tankers.

REPORT

2025 End-of-Year Shipping Market Report

All information provided is for informational purposes only. To the extent that any provided information is based on Veson Data, Veson excludes to the extent permitted by law all implied warranties relating to fitness for a particular purpose, including any implied warranty that Veson Data is accurate, complete, or error free. Veson Data are collated and processed by and on behalf of Veson in accordance with methodologies and assumptions published and updated by Veson from time to time which do not take into account particular circumstances applicable to individuals and therefore; (i) are made available on an ‘as is’ basis; (ii) are not intended as a substitute for formal valuations; (iii) should not be used solely as trading, investment, or other advice; and (iv) are not intended as a substitute for professional judgement. To the extent permitted by applicable law, Veson shall have no liability to party for any errors or omissions in the content of the information provided.