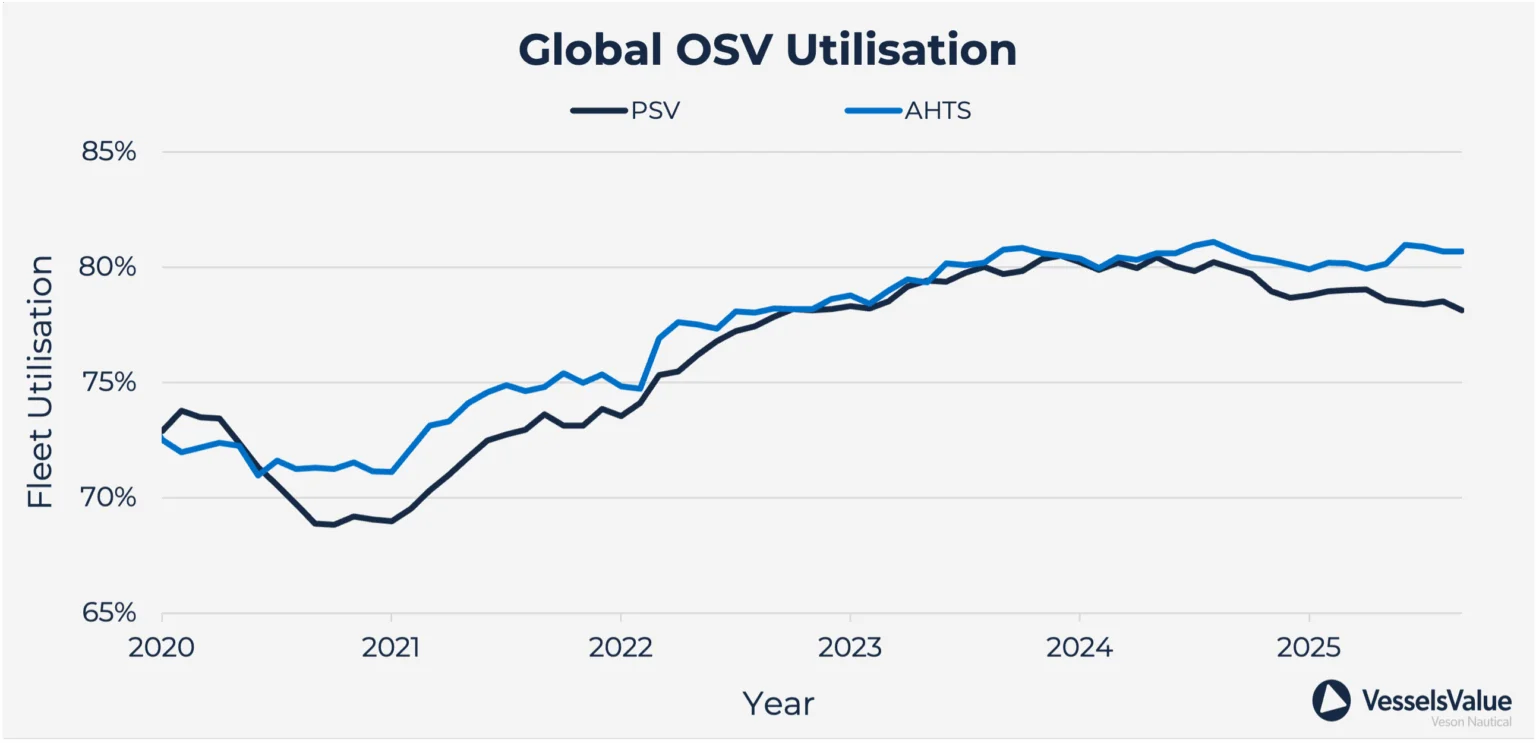

The Offshore Support Vessel (OSV) market has experienced strong growth in recent years. Both 2023 and 2024 saw healthy utilisation and firming rates across key regions, lifting sentiment after years of a weak market following the oil price crash in 2014. Stronger activity as a result of rising oil prices in 2022 pushed global utilisation for both PSV and AHTS fleets to c.80% over the past couple of years—upwards from c.70% at the time of the COVID pandemic. Earnings and valuations have followed a similar upward trajectory since 2022.

However, 2025 has proven more subdued than anticipated. PSV utilisation has eased to c.78%, while AHTS has remained closer to c.80%. Macroeconomic pressures and delays in offshore E&P (Exploration and Production) activity have led to softer demand, with rates below expectations in some regions. This is particularly evident in the North Sea, where day rates have been among the weakest globally with high availability of vessels and limited contracts.

Looking ahead, activity and utilisation are expected to improve in 2026/27 as offshore E&P spending is forecast to increase. This growth will support stronger operator budgets and a growing pipeline of projects, which should tighten vessel supply and lift rates across most regions.

Valuations continued to rise in 2025, though at a far more measured pace compared to the sharp gains seen in 2023 and 2024. During the summer, the Industrial and Commercial Bank of China (ICBC) placed 14 offshore vessels up for auction, with several units struggling to attract buyers due to the steep reactivation costs associated with laid-up tonnage. A notable sale in July saw Large PSV Bourbon Rainbow change hands for USD 23.58 mil to Trinidad based Inland and Offshore Contractors, VV Value USD 23.66 mil. This asset has firmed by only c.9% since the start of 2025, in contrast with the c.74% increase between early 2023 and the end of 2024. This illustrates slower momentum in the OSV sector this year, reflecting a market that remains supported but more toned down than in the preceding two years.

The global fleet is also approaching a turning point. Major owners such as Tidewater, Bourbon, and COSL are operating fleets with average ages of around 14–15 years. As stricter safety and efficiency requirements come into play, many of these units will face retirement or require costly upgrades, underlining replacement needs across the sector.

There has been some newbuilding activity over the past couple of years—notable orders can be seen with the 8 PSVs for Capital Offshore scheduled for 2026–27 and more than 20 PSVs contracted to be built in Brazil for 2027–28. However, newbuilding activity remains modest compared with previous cycles; yard capacity constraints and limited access to capital are keeping order volumes low, ensuring that supply growth remains tight in the near term. Ordering levels are expected to increase more visibly towards the end of 2026 and into 2027 as fleet renewal pressures intensify and improved market confidence supports fresh investment, but this new tonnage will not hit the water in time to ease short-term supply constraints.

Against this backdrop, 2025 looks set to be a year of softer utilisation and rates compared with the peaks of 2023–24. Yet as Offshore E&P investment is forecast to accelerate from 2026 onwards, the combination of an ageing fleet, restricted new supply, and a growing pipeline of projects should see the market lift utilisation and support a renewed firming of day rates and values through the medium term.