The Bulker market has seen significant activity over the past 12 months. Using VesselsValue data, a Veson Nautical solution, we secondhand and newbuilding market trends, including S&P volumes, the most active buyers and sellers by value, and the highest-value vessel currently on order.

View the full infographic below for a complete breakdown of the data.

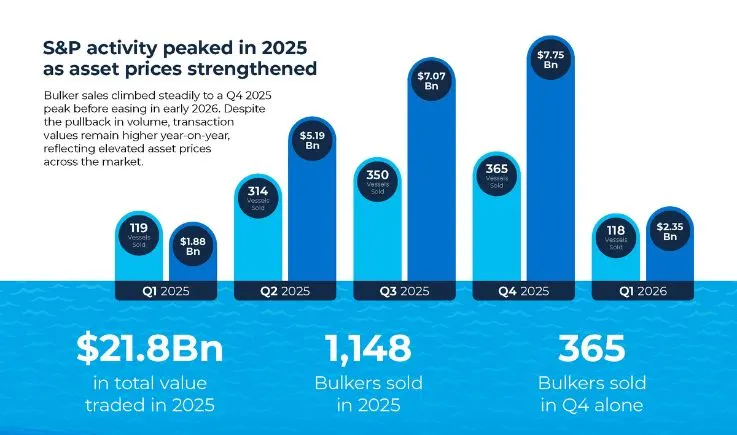

Sale and purchase activity gathers significant momentum

Bulker S&P activity gathered significant momentum through 2025, with both vessel count and vessel value rising steadily across the year. From 119 vessels and USD 1.9 bil in Q1, activity accelerated sharply into Q2 (314 vessels, USD 5.2 bil) and continued climbing through Q3 (350 vessels, USD 7 bil) before peaking in Q4 at 365 vessels at USD 7.8 bil. Q1 2026 has pulled back to 118 vessels and USD 2.3 bil, roughly in line with Q1 2025 levels on vessel count, though transaction value is marginally higher, reflecting the elevated asset prices that characterised the latter half of 2025. With the quarter not yet complete, the full picture for Q1 2026 remains to be seen.

The most active buyers and sellers

Over the last 12 months, Golden Ocean Group emerged as the most active Bulker buyer by value, acquiring 15 vessels for a combined USD 632 mil. Three Chinese leasing companies followed closely: CITIC Financial Leasing and CMB Financial Leasing each purchased 11 vessels, at USD 617 mil and USD 603 mil respectively, while ICBC Financial Leasing secured 7 vessels for USD 457 mil. Japanese operator Doun Kisen rounded out the top five, acquiring 6 vessels for USD 344 mil. The dominance of Chinese financial institutions across four of the five positions underscores the continued appetite for Chinese leasing companies with Bulker tonnage, with the three firms collectively accounting for USD 1.68 bil in acquisitions.

Bocimar was the most active Bulker seller over the past 12 months, disposing of 16 vessels for a combined USD 911 mil — the highest disposal value across any single owner in the period. 2020 Bulkers is also featured among the top five sellers despite a comparatively modest vessel count, offloading 6 vessels for USD 427 mil, pointing to selective monetisation at favourable asset values. Three Chinese entities, ICBC Financial Leasing, COSCO Shipping Specialized Carriers, and Shandong Shipping Corporation, accounted for a combined USD 1.65 bil across 40 vessels, reflecting active portfolio turnover among Chinese owners rather than outright fleet reduction.

The most valuable vessel is a 325,000 DWT Capesize ore carrier which is currently on order. The vessel has been contracted by Shandong Shipping Corporation at Qingdao Beihai Shipbuilding Heavy Industry and valued at USD 150.58 mil with a 2027 delivery, reflecting sustained demand for large-scale ore-carrying capacity.

Top shipowners leading the Bulker fleet

COSCO Shipping Bulk dominates the Bulker fleet both by vessel count and value, operating 261 vessels with a combined fleet value of USD 10.72 bil — more than double the next largest owner by value. Over a quarter of COSCO Shipping Bulk’s fleet is in the Capesize sector, with almost half falling in the Panamax sector and above, reflecting a fleet geared towards larger, higher valued vessels with an average age of nine years. By vessel count, Star Bulk Carriers and Wisdom Marine Lines follow with 142 and 128 vessels respectively, though neither features in the top five by value, suggesting a fleet weighted towards smaller or older tonnage. Nissen Kaiun ranks fourth by count with 123 vessels but second by value at USD 5.51 bil. Bocimar appears in both rankings, 93 vessels valued at USD 4.67 bil. COSCO Shipping Development rounds out the top five by value at USD 4.39 bil, underlining the scale of Chinese state-owned interests across the Bulker sector.

The Bulker market has demonstrated considerable strength over the past 12 months, with S&P volumes and asset values reaching multi-year highs. Chinese owners continue to drive a significant share of market flow on both sides of transactions, with fleet values remaining elevated in 2026 to date. Large-scale newbuilding orders at the top end of the market reflect sustained appetite for high-capacity tonnage, while Q1 2026 activity remains in line with seasonal norms following a particularly active 2025.

Veson_InfoG_BulkerOwnership