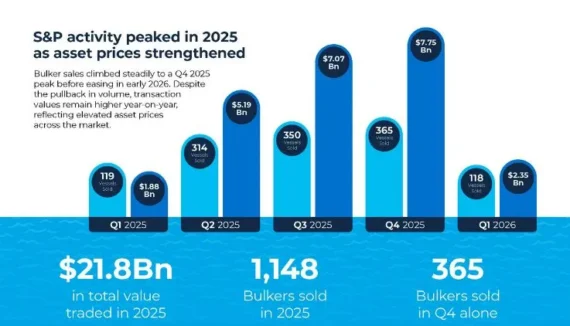

The dry bulk market entered 2026 with a stronger-than-expected start. January rates came in well above seasonal norms across all vessel classes, a strong early signal for the year ahead. Despite structural headwinds, China’s economic slowdown, a coal trade decline, and lingering trade policy uncertainty, shifting trade patterns appear to be reshaping commodity flows supporting ton-mile demand growth.

More recently, escalating geopolitical tensions in the Middle East have added a new layer of complexity — one that could further influence routing patterns and freight rates as the year progresses.

In collaboration with VP of Valuation & Analytics Matt Freeman, our latest Market Insights report, Dry Bulk Finds Growth Amid Global Uncertainty in 2026, examines these emerging trends and where the key risks and opportunities lie across dry bulk markets.

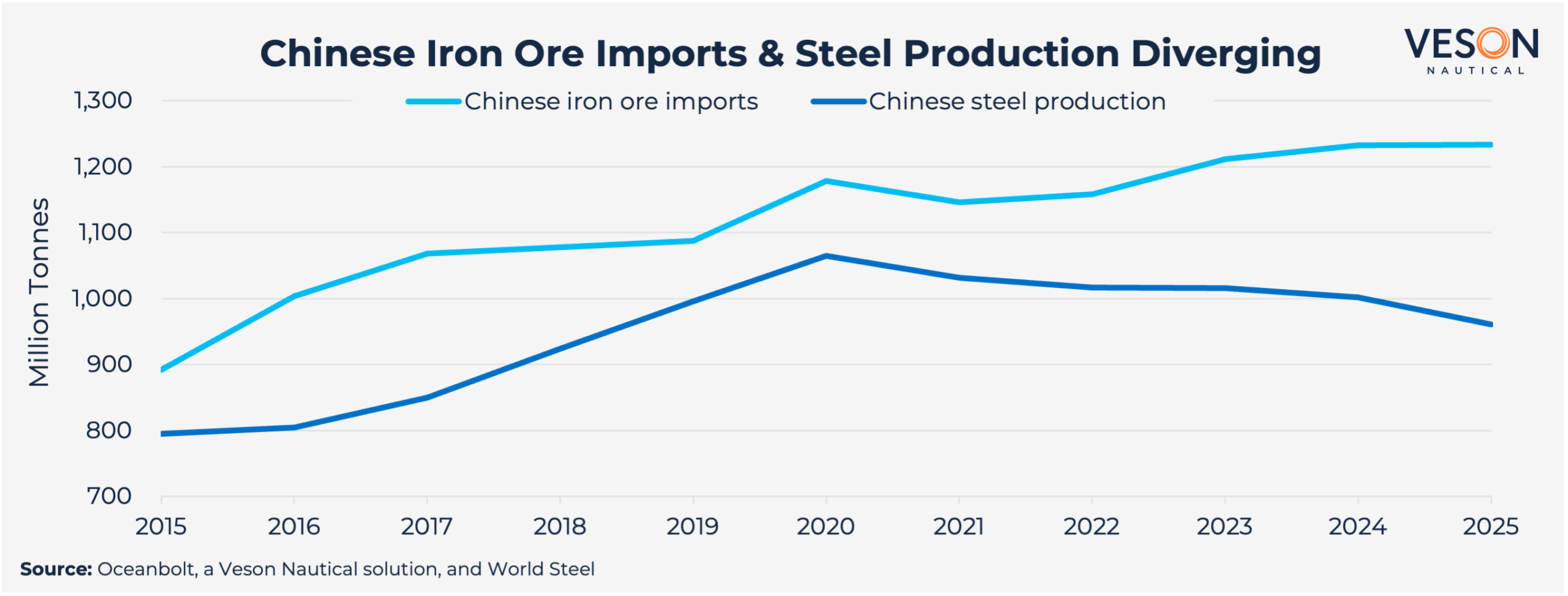

A paradox at the heart of iron ore trade

China’s steel production has been in decline since 2021, yet seaborne iron ore imports reached a record 1.23 billion tonnes in 2025 — a divergence that reflects strategic stockpiling and falling domestic ore output.

As the chart below illustrates, imports and steel production have been moving in opposite directions for several years now.

Looking ahead, the commissioning of Guinea’s Simandou iron ore mine in late 2025 introduces a notable geographic shift in global supply. With sailing distances from Guinea to China roughly three times longer than from Australia, the ton-mile implications are significant and could reshape Capesize demand this year and beyond.

“There are positive signals for commodities carried by Capesizes, but the valuations are moving faster than the market,” Matt reinforced at Veson’s recent Geneva Summit.

The full report explores what this means for asset values across vessel segments.

A mixed picture for coal, minor bulks, and grains

Seaborne steam coal trade declined c.5% in 2025, driven by renewable energy expansion in China and aggressive domestic production growth in both China and India. This pressure appears likely to continue in 2026, though growing demand across Southeast Asia may provide a partial offset.

On the minor bulks side, investment in green energy infrastructure is proving supportive. Chinese bauxite imports surged 27% in 2025, with Guinea emerging as the dominant supplier following Indonesia’s export ban — another long-haul trade route with meaningful ton-mile value. Strong demand for minor bulks, combined with China’s pivot toward steel exports amid weaker domestic demand, has also been a key tailwind for the Supramax segment.

In grain markets, the US-China trade truce provided a meaningful boost to agricultural trade flows, with forward-looking cargo data from Shipfix already showing a sharp recovery in US-to-China bookings. This is particularly positive for the Panamax segment, which had a challenging 2025 weighed down by China’s record domestic grain harvest and the suspension of US soybean purchases amid trade tensions.

Constructive 2026 outlook, supported across segments

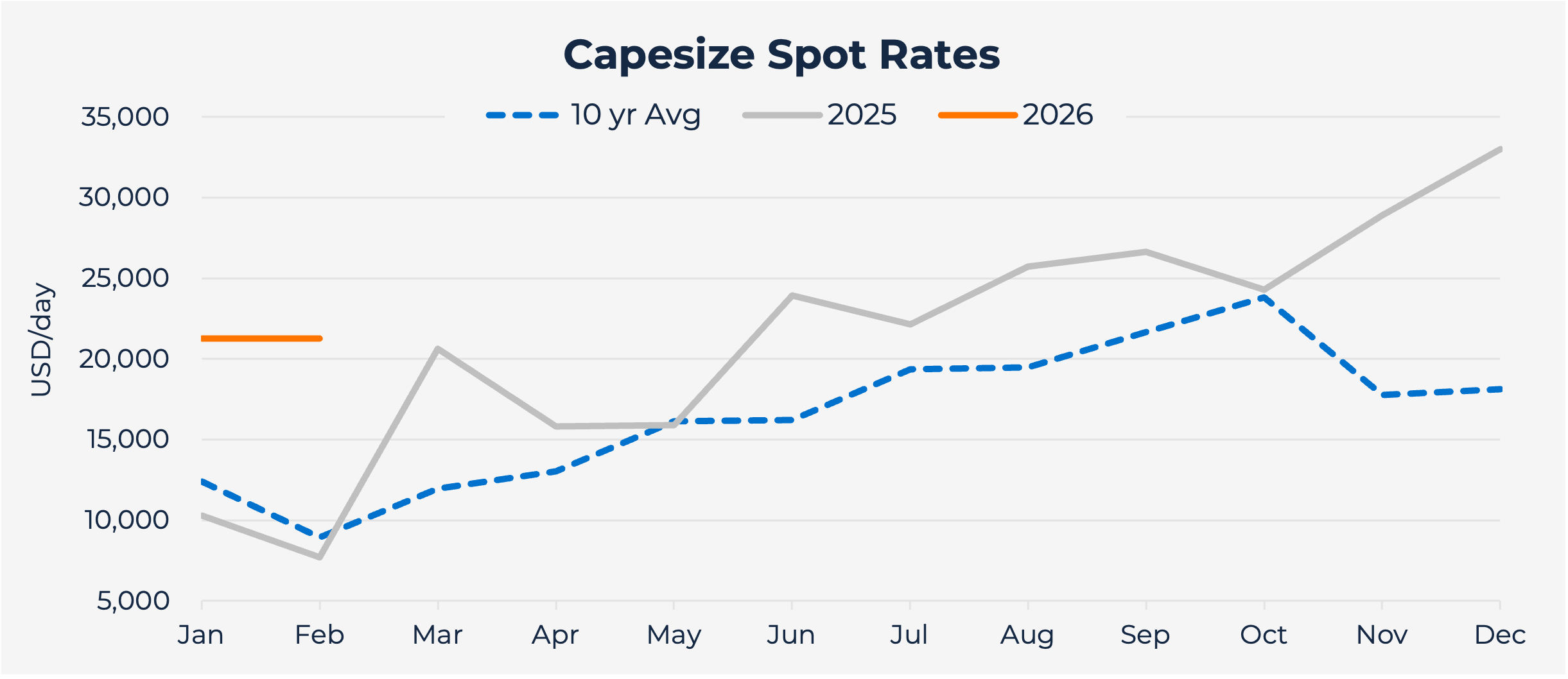

January is historically the weakest month of the year for dry bulk, yet Capesize vessels averaged $21,250/day, 72% above the 10-year average for the month. Additionally, Panamax, Supramax, and Handysize all exceeded their decade averages by 17–27%. This broad-based strength is a powerful leading indicator of sustained momentum ahead.

While uncertainty remains around China’s trajectory, evolving trade policy, and the fluid situation in the Middle East, the early evidence is encouraging. Continue reading about these key drivers in the full Market Insights report.