Overview

The global shipping market enters 2026 characterized by exceptional volatility across sectors, with geopolitical disruptions and structural supply-demand imbalances creating divergent outlooks.

Tanker markets are experiencing historic quarterly earnings levels not seen since 2008/2009, supported by OPEC+ production increases, sanctions-induced inefficiencies, and floating storage dynamics that have tightened effective supply. The Bulker sector has returned to normal seasonality following years of disruption, benefiting from tight supply conditions and emerging ton-mile support from new Atlantic basin iron ore sources, particularly Guinea’s Simandou mine. Container and LPG markets continue to demonstrate firm freight rates despite substantial vessel deliveries, as Red Sea diversions and operational speed reductions absorb capacity; However, all sectors face mounting fleet growth pressures from historically elevated orderbooks, with Container vessels representing the primary driver of global shipyard activity at 4.6 mil TEU ordered in 2025.

The looming normalization of Red Sea transits and potential resolution of the Russia-Ukraine conflict represent significant downside risks to ton-mile demand, whilst China’s structural economic transition from construction-led to high-tech growth creates long-term uncertainty for commodity-dependent shipping segments.

If you’d like a deeper dive into any of the market sectors, speak to an expert to learn more about our forecasting services.

Here is a summary of where the major markets could be heading:

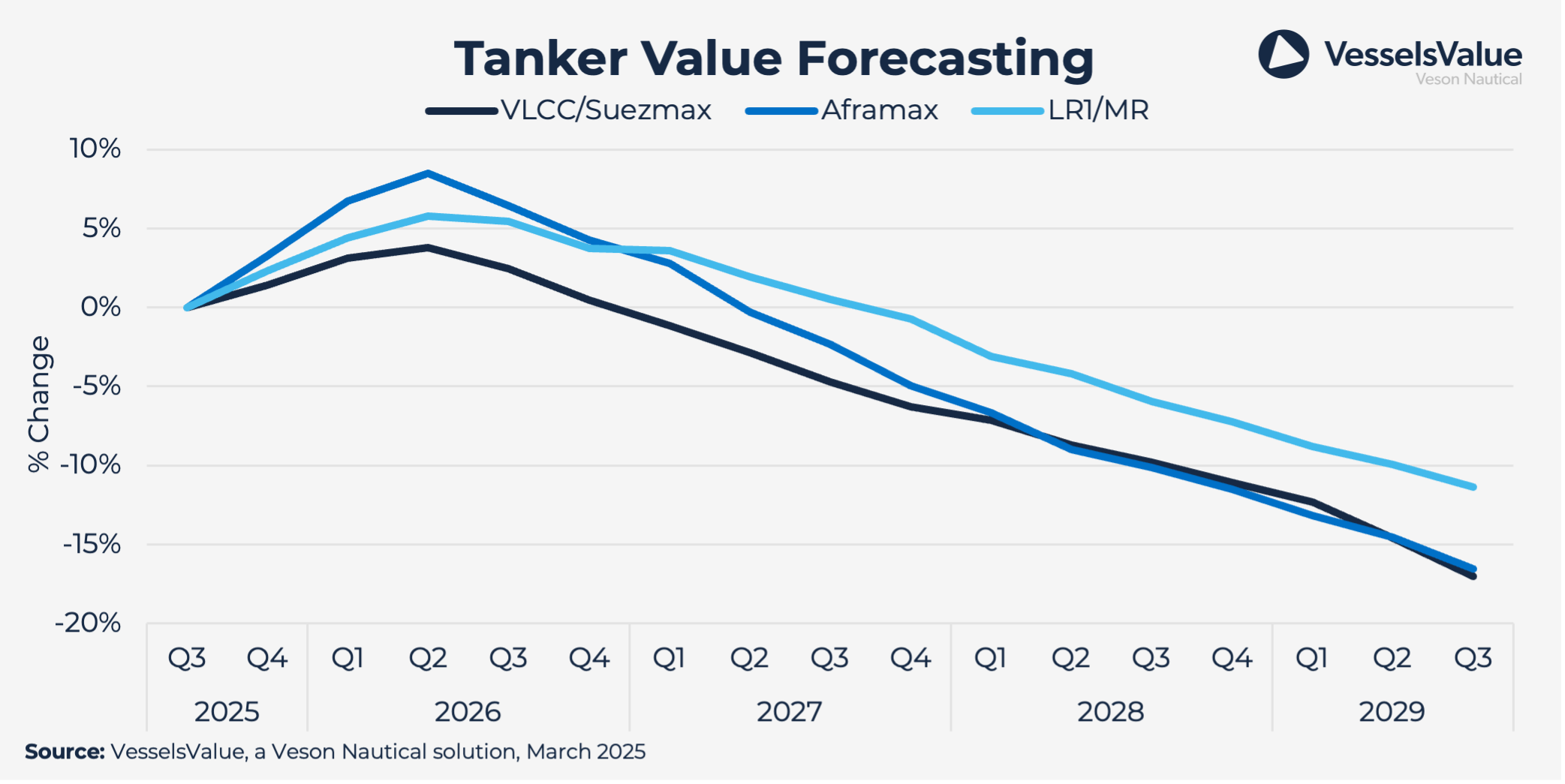

Tankers

- VLCC earnings surged to over 100,000 USD/day in Q4 2025, the highest quarterly levels since 2008/2009, driven by OPEC+ production increases, South American supply growth, and sanctions-related floating storage

- Product Tanker markets show mixed performance with MRs approaching 30,000 USD/day whilst LR segments disappoint despite refinery switching; EU ban on Russian product imports from January 2026 will disrupt flows

- Long-term outlook remains constructive as crude production centers further from demand (MEG and Atlantic growth) despite potential headwinds from Ukraine peace deal and Red Sea normalisation

- Newbuilding ordering increased quarter-over-quarter in 2025 with Q4 being the most active, though total 45.4 mil DWT ordered represents 27% decline versus 2024; product Tanker ordering down 66% whilst crude ordering maintained parity with previous year

- Fleet growth accelerating with deliveries expected to nearly double in 2026 to 38 million DWT, whilst orderbook stands at 17% of fleet with scrapping yet to materialise significantly

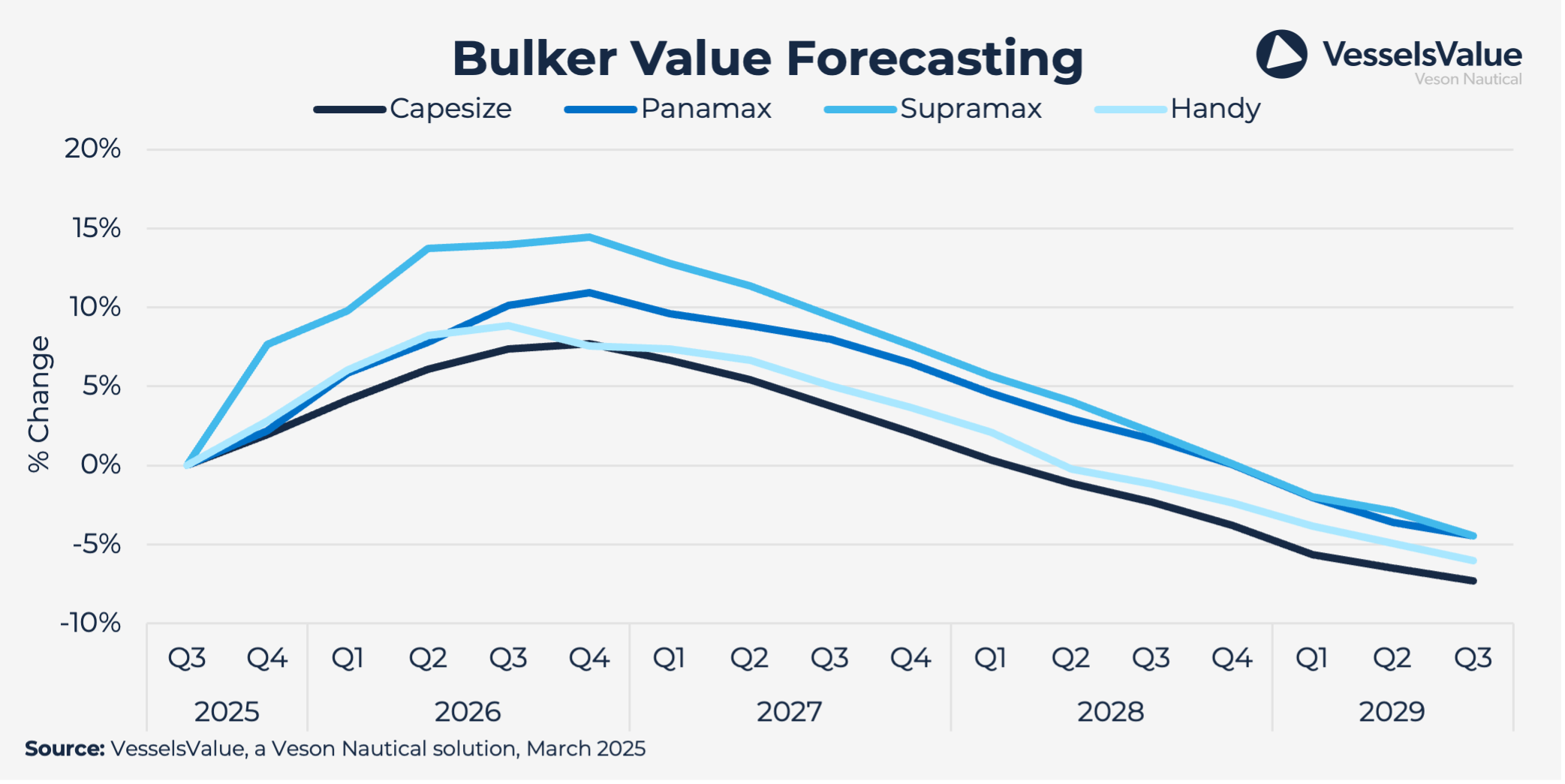

Bulkers

- Market returned to normal seasonality in 2025 with strong Q4 peak; Capesize rates reached 45,000 USD/day on robust Chinese iron ore and bauxite demand from Atlantic basin before seasonal decline

- Guinea’s Simandou mine commenced shipments with 120 mil tons annual capacity creating substantial ton-mile support as distance to China is three times longer than Australian routes

- Structural headwinds emerging as Chinese steel production faces decline amid economic transition from construction to high-tech; seaborne coal trade declining due to decarbonisation and import substitution in China/India

- Minor bulk commodities providing growth offset to coal decline, with Guinea-China bauxite trade surging 40% in 2025 to support aluminium production; energy transition demand for materials like copper, nickel, and aluminium expected to continue rising alongside green infrastructure investment

- Fleet growth averaging 3.5% annually expected to gradually outpace demand growth beyond 2026 despite current tight market conditions and 40% decline in newbuilding orders during 2025 ciency.

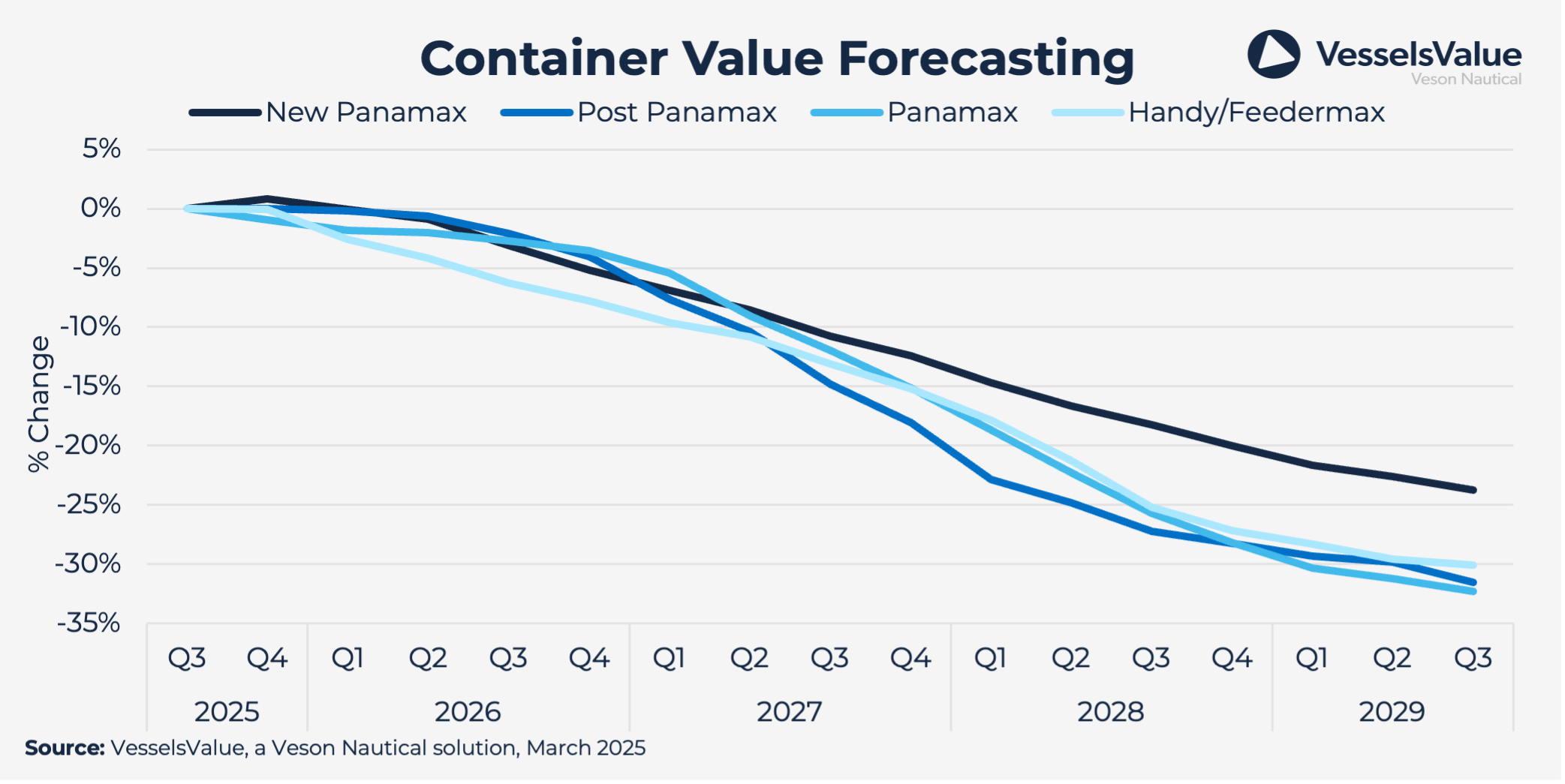

Containers

- Freight rates remained firm in Q4 2025 (up 14.3% year-on-year) despite 1.9 mil TEU deliveries as carriers reduced speeds 1.8% to support rates; tariff truce provides temporary relief for US-Asia volumes

- TEU-mile demand expected to decline 1.3% in 2026 as Red Sea normalisation progresses throughout year, followed by 2% average growth 2027-2029 supported by Chinese export expansion

- Severe supply-demand imbalance looming with 11.6 mil TEU orderbook (35.5% of fleet) and 9.5% average net fleet growth forecast 2026-2029, driving freight rate declines of 8.5% in 2026 and 17.6% in 2027

- Strong ordering activity continued with 4.6 mil TEU placed in 2025, surpassing 2024 levels; sustained container vessel demand maintains elevated shipyard utilisation and extended delivery schedules, keeping newbuilding prices above historical averages across all segments

- Scrapping remains minimal (0.25 mil TEU since 2023) but expected to increase moderately in sub-3,000 TEU segment as older vessels become uneconomical

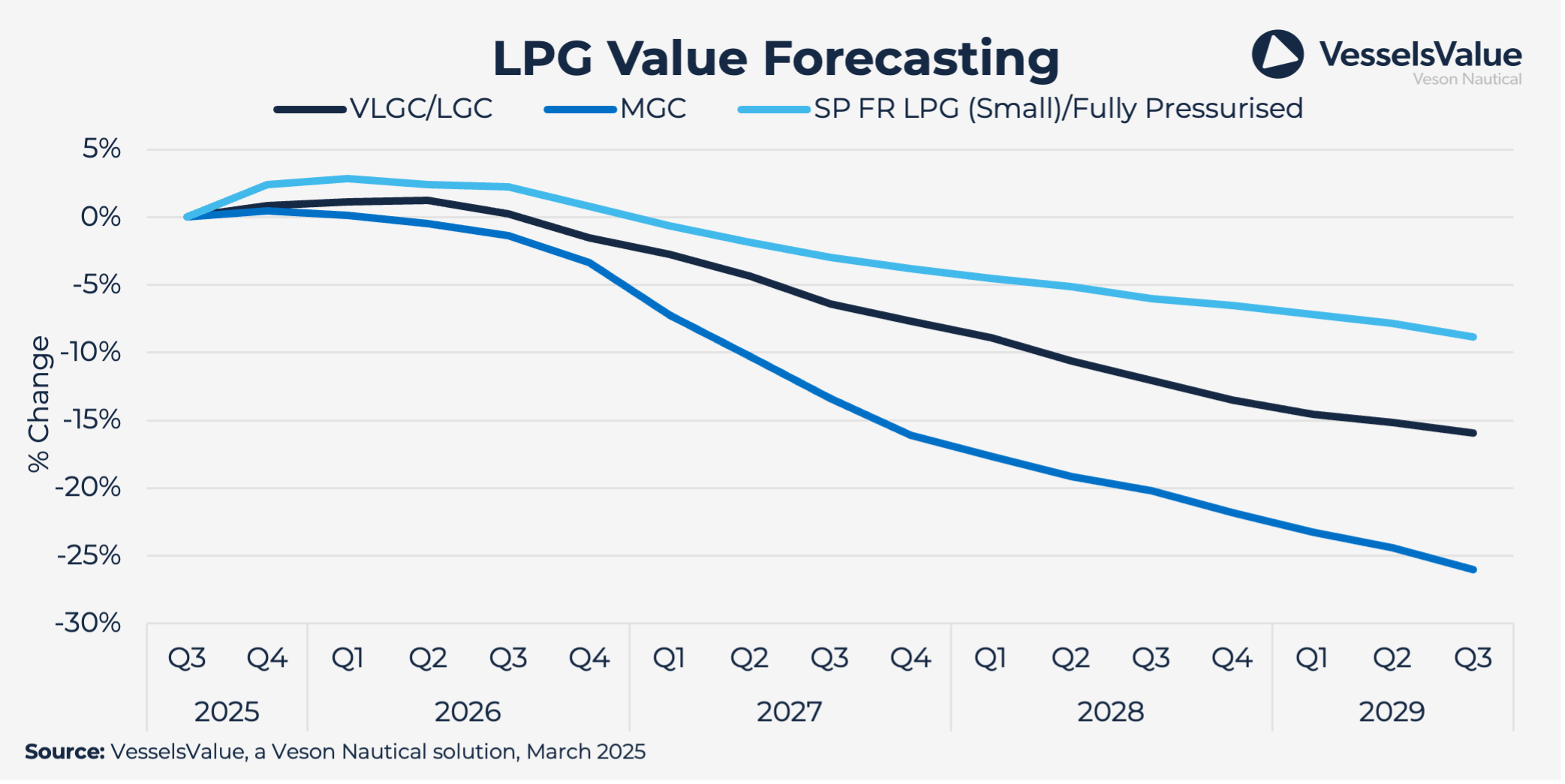

Gas

- VLGC earnings averaged 55,000 USD/day in Q4 2025 (up 45% year-on-year), supported by 6% growth in US propane exports and 4.9% production increase; full-year 2025 earnings reached 50,000 USD/day

- US and Middle East export growth expected to continue with terminal expansions supporting US volumes and new LNG projects increasing MEG LPG availability (5.5% average regional growth forecast)

- Fleet growth pressures mounting with VLGC net fleet expansion of 7.3% annually forecast 2026-2029; MGC segment faces acute pressure with 50% orderbook-to-fleet ratio and 11.6% average growth

- Earnings expected to remain firm in 2026 backed by export volume growth but likely decline from 2027 onwards as vessel deliveries outpace demand; Panama Canal normalised but congestion risks remain with fleet expansion

- Ammonia trade showing renewed growth with 4% increase in 2024 and 2% in 2025, though substantial expansion unlikely near-term due to delays and cancellations in blue/green ammonia projects; ethylene trade expected to recover in forecast period benefiting ethylene-capable vessels

WEBINAR

Dry Bulk & Tanker Trades: Year-End Review & 2026 Outlook

All information provided is for informational purposes only. To the extent that any provided information is based on Veson Data, Veson excludes to the extent permitted by law all implied warranties relating to fitness for a particular purpose, including any implied warranty that Veson Data is accurate, complete, or error free. Veson Data are collated and processed by and on behalf of Veson in accordance with methodologies and assumptions published and updated by Veson from time to time which do not take into account particular circumstances applicable to individuals and therefore; (i) are made available on an ‘as is’ basis; (ii) are not intended as a substitute for formal valuations; (iii) should not be used solely as trading, investment, or other advice; and (iv) are not intended as a substitute for professional judgement. To the extent permitted by applicable law, Veson shall have no liability to party for any errors or omissions in the content of the information provided.