China’s shipbuilding industry continues to dominate the global orderbook, and the past year has seen its top yards cement their grip on global contracting. The top 10 Chinese yards have collectively attracted significant newbuilding investment across a broad range of vessel types, from VLCCs and LNG carriers to Containers and Bulkers.

Below, we profile the leading yards by order volume, highlighting the deals, vessel preferences, and values that define each yard’s position in today’s market.

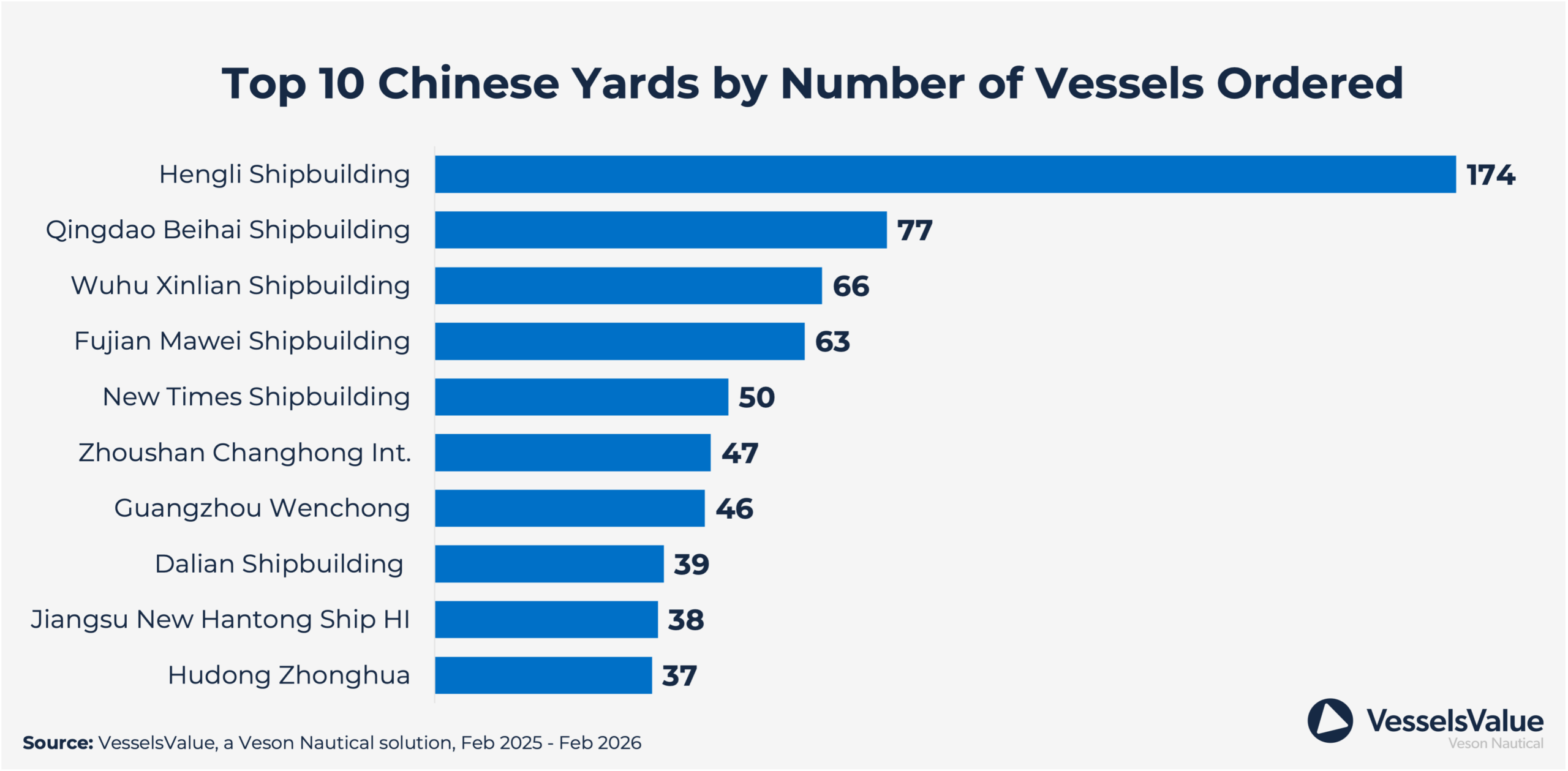

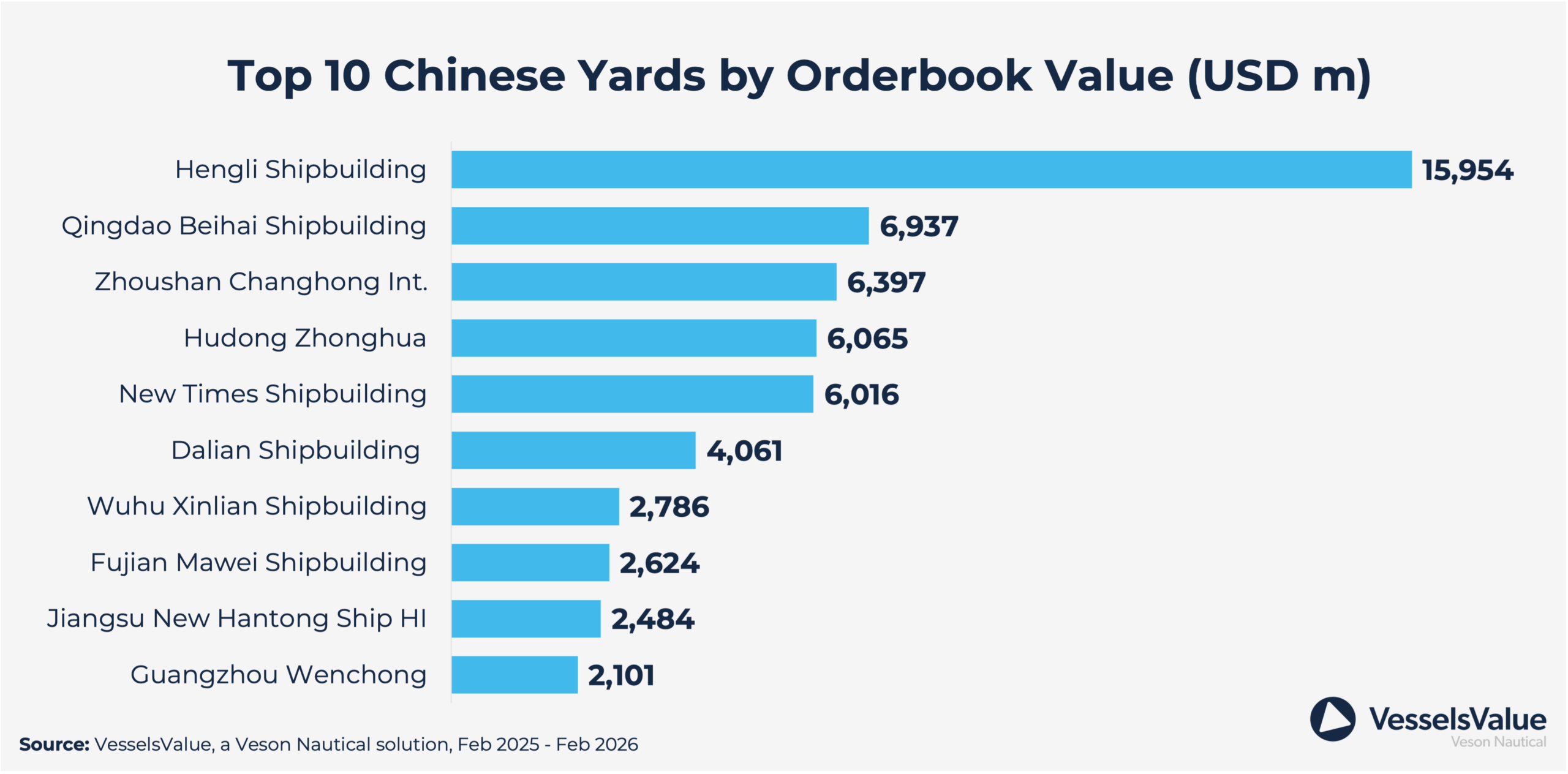

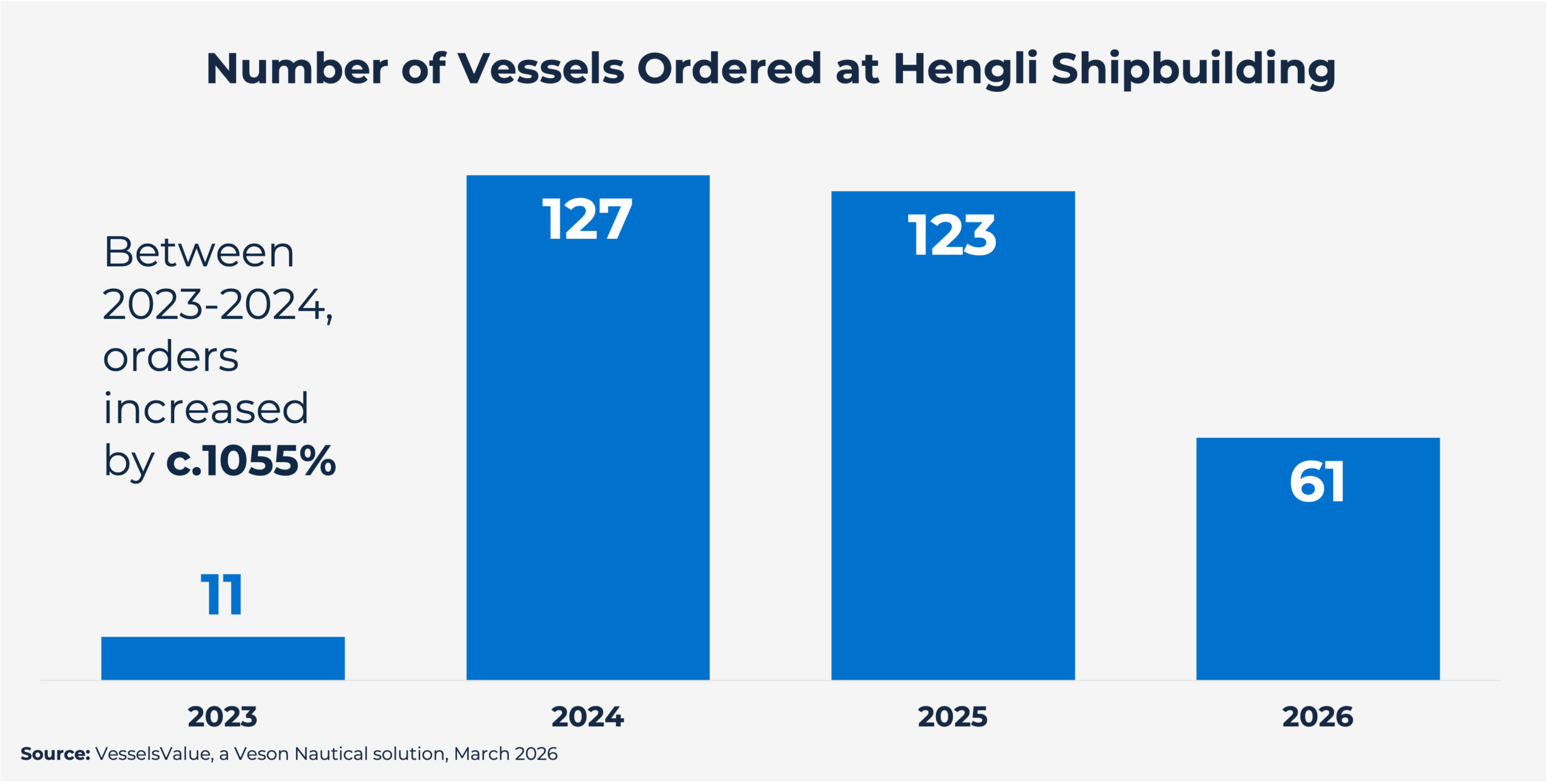

Over the last year, Hengli Shipbuilding tops the list significantly ahead of the competition with 174 orders received, valued at USD 16 bil. Impressively, Hengli Shipbuilding is a relatively new yard, established in the early 2020’s, having taken over the former STX Dalian shipyard on Changxing Island, Dalian.

VLCCs are the vessel of choice at this yard, representing c.31% of en bloc orders. Most recently, Capital Maritime and Trading ordered 11x 306,0000 DWT VLCCs scheduled to be delivered in 2028-2029 and contracted for USD 120 mil each, VV value USD 122.56 mil each.

LR2 Tankers are the second most popular vessel ordered at c.15% and in third place, Post Panamax Containers with a share of c.12%.

Qingdao Beihai Shipbuilding are second in the list of top Chinese yards, having received 77 new orders since February 2025, valued at USD 6.9 bil.

The orders at this yard have focussed heavily on the Capesize sector, comprising 31 of the 49 Newcastlemaxes (around 210,000 DWT) ordered by COSCO Shipping Bulk. These vessels are set to be delivered between 2027- 2031.

In addition, Qingdao Beihai is constructing 10 Ore Carriers of 325,000 DWT, contracted by Shandong Shipping Corporation and slated for delivery between 2027-2029. These vessels are contracted for USD 130 mil each, VV value USD 133.69 mil each. These vessels are being built with dual fuel methanol specifications and have been entered into long-term timecharter agreements with Brazilian Iron ore major, Vale.

Wuhu Xinlian Shipbuilding are in third place with 66 vessels ordered over the last year, valued at USD 2.8 bil. The most popular vessels at this yard were in the Ultramax and Small Handy Bulker sub sectors accounting for c.31% and c.15% respectively. Notable deals include 10 x Ultramax Bulkers ordered by Huaxing Shipping for delivery between 2027-2029, contracted for USD 29.5 mil each en bloc, VV value USD 25.76 mil each.

Fujian Mawei Shipbuilding rank fourth with 64 newbuilding contracts received but ranking further down the list in value terms with USD 2.6 bil.

The majority of orders at this yard are in the Panamax Bulker (c.46%) and Handy Container (c.37%) sectors. This orderbook includes 30 x Panamax Bulkers ordered by COSCO Bulk Carrier in June 2025, scheduled for 2026-2029 delivery and contracted for USD 50 mil each en bloc, VV value USD 49.66 mil each. Eighteen 1,800 TEU Handy Containers were ordered in August 2025 by Eastern Pacific Shipping; the vessels are set to be delivered between 2027-2029 and contracted for USD 33 mil each en bloc, VV value USD 30.56 mil each.

New Times Shipbuilding are in fifth place with 50 vessels ordered and valued at USD 6 bil. A notable mention also goes to Hudong Zhonghua, who rank fourth in terms of value with a total investment of USD 6 bil for 37 vessels ordered last year. This is due to the large number of high-ticket vessel types on order where Large LNG vessels account for the largest proportion of orders at c.35%, followed by VLCCs at c.30%.

China’s top yards are clearly firing on all cylinders, with orderbooks stretching well into the decade and contract values reflecting sustained demand across multiple vessel segments. Hengli’s meteoric rise, Hudong Zhonghua’s high-value portfolio, and the sheer breadth of activity across the remaining yards paint a picture of an industry operating at full capacity and showing little sign of slowing down.