Tanker newbuild ordering has gathered significant momentum through 2026, increasing c.358% year-on-year with 444 vessels placed year to date (including on order and options) across all major segments. Activity peaked in February at 20.5 mil DWT before moderating in subsequent months.

Ordering has skewed heavily towards large crude carriers, with VLCCs and Suezmax vessels commanding the lion’s share of activity. A handful of dominant owning nations accounted for the bulk of commitments, reflecting a confident bet on long-term Tanker demand.

Using VesselsValue data, we analyzed the top ordering trends, vessel types, and owning nations shaping the Tanker newbuild market this year.

Tanker newbuild ordering activity

The newbuilding market slowed significantly through 2023 and 2024 amid heightened sanctions activity. Then, following the relaxation of Trump tariffs in early 2026, new orders surged. Last year, around 10 to 15% of the VLCC fleet was on order, while that figure now stands at 25%, signaling a significant pipeline of new tonnage that will hit the water in the coming years.

While newbuild VLCC prices are significant at USD 131.4 mil, the economics are underpinned by an exceptionally tight market. Vessel supply remains constrained and both spot and time charter rates are elevated, with one-year TC rates currently around 102,000 USD/day giving charterers confidence to take positions on forward delivery and allowing owners to write down a substantial portion of the asset cost before the vessels enters service.

For owners with ageing fleets, near-record asset valuations have created a further opportunity to sell older tonnage and reinvest in younger, more fuel-efficient vessels. Dynacom is a notable example, having sold 16 vessels in the last six months while placing 36 newbuild orders since the start of the year.

VLCCs dominate the February ordering surge

Tanker ordering in 2026 to date has been firmly anchored in the larger crude segments, with VLCCs and Suezmax vessels accounting for over half of the 353 total orders placed. VLCC ordering alone has more than doubled compared to the same period in 2025.

The Tanker orderbook has expanded significantly over the past year, with vessels on order as a proportion of the live fleet rising from an average of 15% in May 2025 to 33% in May 2026. The most marked shift has been in VLCCs, where the on order proportion has nearly tripled from 12% to 33% of the live fleet, while Suezmax has risen from 20% to 37%. LR2 remains the segment with the highest proportion of vessels on order relative to the live fleet at 42%, unchanged year on year, while Aframax on order has edged up from 6% to 8%.

The contrast between the two periods reinforces the scale of the ordering acceleration, with large crude and product Tanker segments carrying a significantly larger pipeline of future tonnage than twelve months ago.

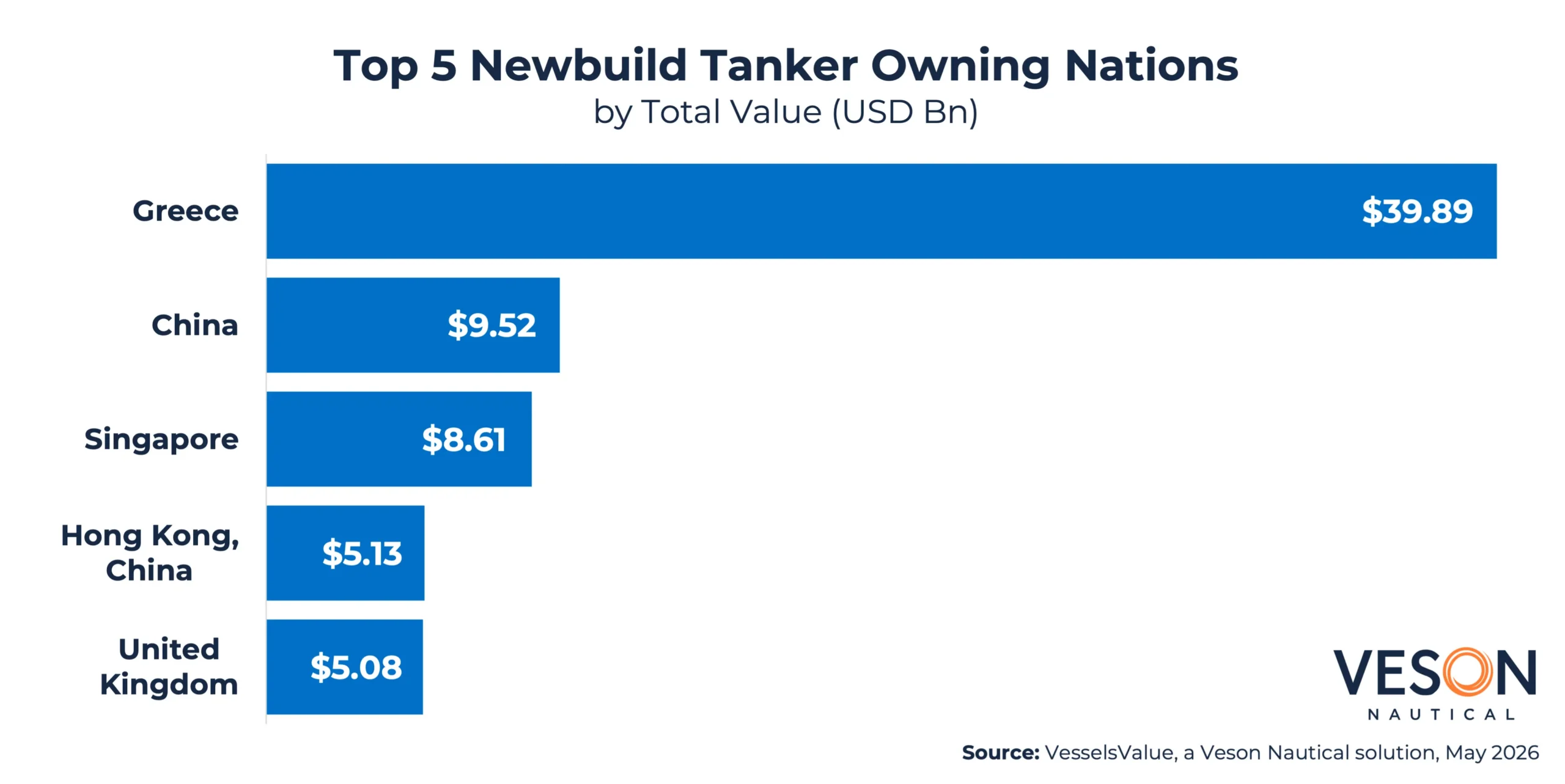

Newbuild Tanker owning nations

Greek owners are driving newbuild Tanker contracting at scale, holding USD 39.89 bil in ordered tonnage and accounting for c.60% of the USD 65.72 bil combined total across the top five owning nations. China ranked second at USD 9.52 bil (c.14%), followed by Singapore at USD 8.61 bil (c.11%), Hong Kong, China at USD 5.13 bil (c.8%), and the United Kingdom at USD 5.08 bil (c.7%). Greece’s portfolio is worth more than four times the combined value of the remaining four nations.

With VLCC ordering running at more than double the pace of the same period in 2025 and Greek owners committing close to USD 40 bil to newbuild tonnage, it remains unclear if this level of contracting is sustainable through the reminder of the year. Ongoing uncertainty in the Middle East, particularly around the Strait of Hormuz and its implications for crude trade flows, adds a layer of caution to the outlook. Key factors to monitor include shipyard capacity and pricing, and whether mid-size segments such as Aframax and Panamax begin to close the gap on the larger crude carriers.

REPORT