Recent events in Iran and the Middle East have sent shockwaves through Tanker markets, with conditions rapidly shifting into uncharted territory. The Strait of Hormuz, through which around 20% of global oil exports pass, now sits at the centre of the crisis, with several commercial vessels including VLCCs idling as masters deem approach to the Gulf of Oman too risky.

According to VesselsValue data, 365 VLCCs have passed through the Strait of Hormuz since the start of the year, equating to c.40% of this fleet. 1,049 vessels currently stand in the inner Persian Gulf, spanning Tankers, Bulkers, Containers, LNG, LPG, and Vehicle Carriers with around 8% of the global VLCC fleet presently positioned in the Middle East Gulf.

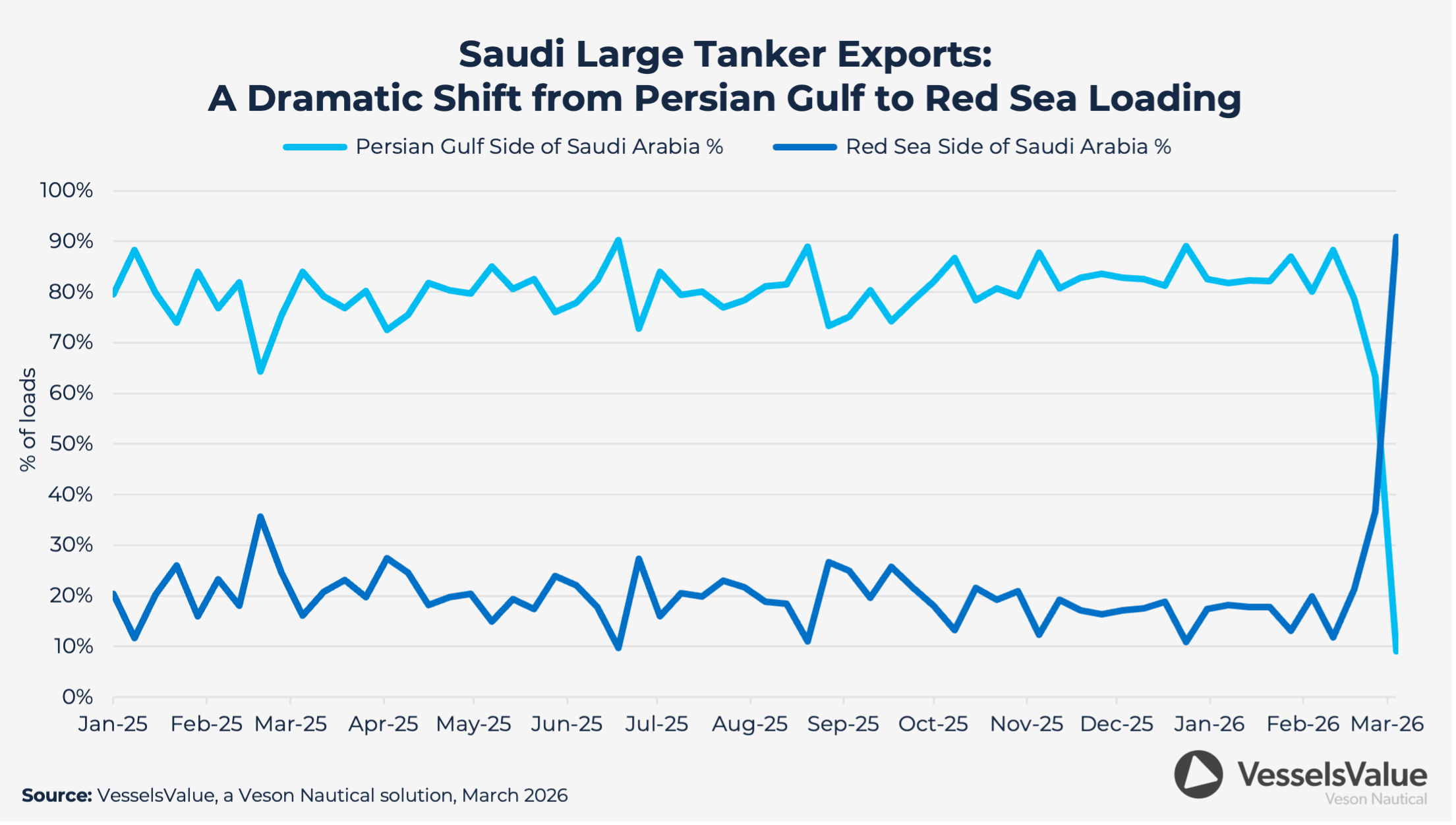

Middle East Gulf loadings of large Tankers from Saudi Arabia, which have accounted for around 80% of total Saudi export volumes throughout 2025, collapsed to just c.10% in the week of 3rd March as the Red Sea’s share rose to c.91%. Total weekly Saudi large Tanker exports also softened to c.2.3 mil MT over the same period, suggesting the conflict is already beginning to weigh on the volume of crude moving through the Gulf.

While pipeline alternatives exist, their capacity is no substitute for the Strait of Hormuz. According to the IEA, only Saudi Arabia and the UAE have bypass routes via the East-West pipeline to Yanbu and the UAE’s Fujairah pipeline respectively. Together, these routes have a combined spare capacity of an estimated 3.5–5.5 mil b/d against the 20 mil b/d that normally transits Hormuz. The East-West pipeline is already being utilised, with Indian refiners reported to be paying premium prices for crude lifted out of Yanbu.

For VLCC demand, these stems still require large Tanker liftings for onward journeys to Asia, meaning pipeline diversion may sustain rather than eliminate VLCC employment, though Red Sea routing carries its own risk given the Houthi threat at Bab al-Mandeb.

Despite the elevated risk environment, Veson’s AIS data confirms that a small number of laden VLCCs have continued to transit the Strait of Hormuz since the crisis escalated, with six vessels recorded passing through between 4th and 9th March. While this demonstrates the waterway has not been fully closed, it represents a dramatic contraction from the 365 VLCCs that transited in the year to date.

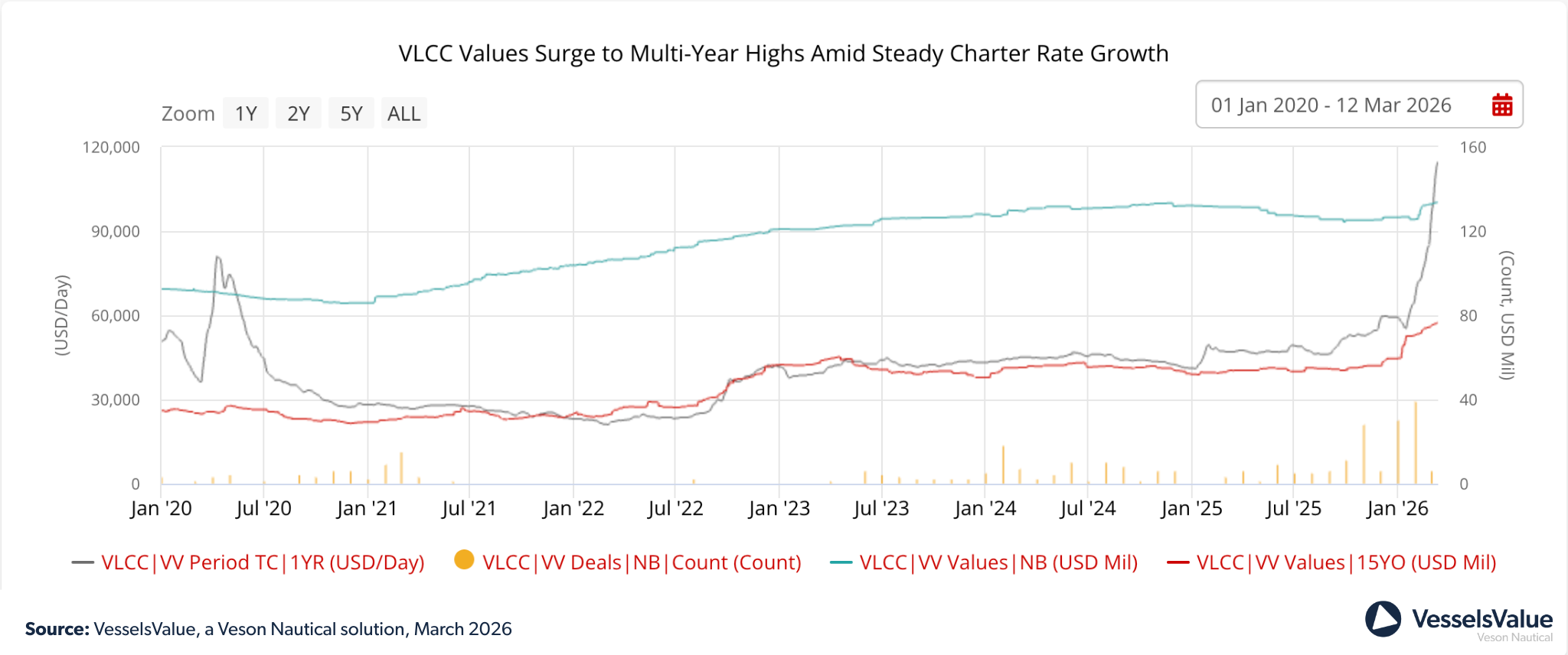

This disruption is already being reflected in the market: MEG/China TD3 rates soared to a record high of 485,959 USD/day, as markets grapple with a potential shut-in of Middle East oil volumes. One-year TC rates have surged to almost 111,000 USD/day, surpassing the highs of the 2020 floating storage boom and up c.41% from the start of the year.

Compounding the tightening supply picture, Sinokor’s accelerated fleet acquisition and the progressive removal of sanctioned vessels from effective trading supply are further constraining available tonnage.

The buoyant earnings environment is translating directly into extraordinary newbuilding appetite. In the three months leading up to 25th February 2026, 88 VLCCs were ordered at a combined value of USD 10.4 bil, a staggering increase of 633% year-on-year. Newbuilding values are sitting at their highest levels since August 2009, with 320,000 DWT vessels up c.5.57% since the start of the year from USD 126.67 mil to USD 133.72 mil. Hengli Shipbuilding has emerged as the yard of the moment, accounting for 35 VLCC orders so far this year alone and cementing its position as the busiest Chinese yard over the past twelve months.

Greek owners have been the most active buyers of newbuild tonnage, placing 35 orders year-to-date at a combined value of USD 3.8 bil. Owners who were previously hesitant to commit at elevated yard prices are now moving decisively, driven by an earnings outlook that is increasingly difficult to ignore. With US-Iran tensions escalating and Hormuz disruption risk firmly in focus, the investment case for new VLCC tonnage appears, for now, overwhelmingly compelling.

Secondhand sales activity has surged in parallel, with transactions rising from 14 in the first two months of 2025 to 71 over the same period in 2026, an increase of c.407%. Sinokor has continued its buying spree, bringing its total VLCC acquisitions to 54 vessels, equating to 76% of all VLCC sales so far this year.

On the sellers side, Greek owners have been the most active, accounting for c.28% of sales, followed by Cyprus at c.20% and Belgium at c.11%. Asset values have risen sharply in step with the broader market, reaching their highest levels since August 2008: 15YO vessels of 310,000 DWT have appreciated c.28.47% since the start of the year, from USD 59.57 mil to USD 76.53 mil.

Notable recent sales include the Shaybah (319,400 DWT, Jun 2008, Daewoo), sold DD due by Bahri to Sinokor for USD 59 mil against a VesselsValue assessment of USD 62.29 mil, and the Singapore Spirit (318,700 DWT, Jun 2013, Jiangnan Shanghai Changxing HI), sold by Teekay Tankers to Sinokor for USD 84.5 mil against a VesselsValue assessment of USD 86.59 mil.