The Bulker market entered 2026 with momentum, supported by firm asset values and solid secondhand activity. That momentum has since been tempered by the escalating crisis at the Strait of Hormuz, which has progressively weighed on ordering confidence, freight markets, and transaction volumes as the conflict has deepened.

At the time of writing, 192 Bulkers totalling 11.7 mil DWT are among the 1,005 vessels stranded in the region, including Iranian-owned tonnage. While Capesize vessels have seen some rate support from broader fleet tightening, smaller segments face more direct exposure to disrupted Gulf commodity flows, and the market as a whole is now in a period of cautious reassessment.

Newbuilding orders slow sharply after a strong start to 2026

Bulker newbuilding activity has slowed markedly in 2026. The year opened strongly, with 45 contracts recorded in January and 40 in February, before falling to 25 in March, less than a third of the 85 reported in the same month last year. No sales have been reported so far in April, in contrast to the activity seen at this point in 2025 where 14 vessels were ordered over the same period. Traditionally, March represents a seasonal uptick for Bulkers, and while 2026 began with momentum, the escalation of the Hormuz crisis appears to have weighed on ordering decisions as the quarter progressed.

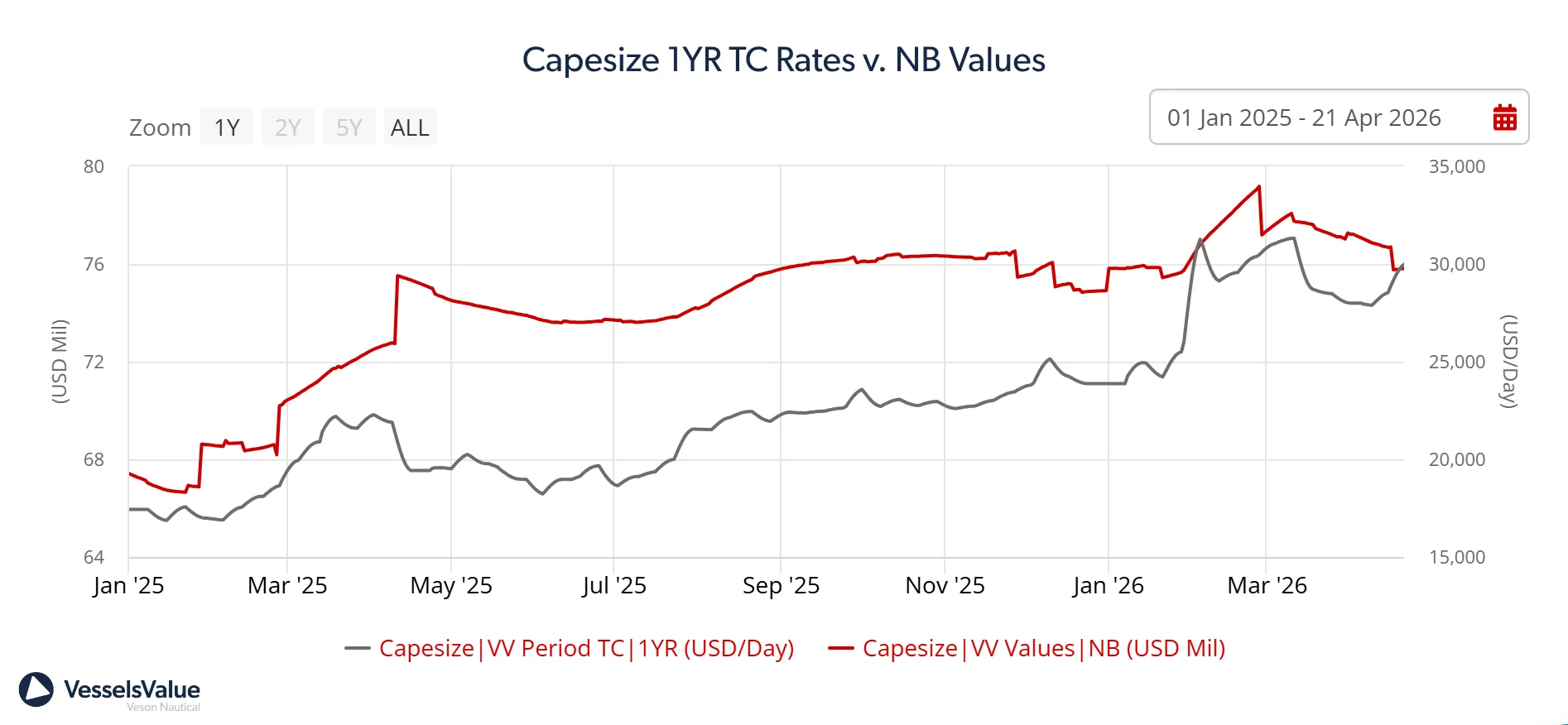

Despite the volume decline, values have held firm. Using VesselsValue Timeseries, we can see that Capesize newbuilding prices for vessels of 180,000 DWT have edged up 1.27% since January to USD 76.87 mil, a signal that asset confidence remains intact even as contracting activity softens. Capesize and Newcastlemax orders have dominated the 2026 orderbook, accounting for 40% of contracts placed this year with 44 units on order. That compares to a 13% share on just 25 sales across the same period in 2025, suggesting owners are concentrating commitments at the larger end of the size spectrum where ton-mile exposure to long-haul disruption is relatively limited.

The broader picture currently more of a ‘wait-and-see’ market, pausing rather than retreating. Elevated asset values point to continued confidence in the medium-term demand outlook, but near-term ordering momentum has clearly lost ground as operators weigh the duration and impact of the Hormuz closure on dry bulk trade flows, a theme that also runs through earnings and secondhand activity.

Capesize earnings climb as smaller segments diverge

Bulker earnings have shown divergence across segments in 2026, with Capesize vessels recording the sharpest moves. Spot rates reached their highest levels of the year in late March to early April, likely a combination of solid underlying volumes and animprovement in sentiment following the ceasefire announcement.

Driven not by direct Hormuz exposure, Capesizes do not trade significantly through the strait, but by a tightening of effective fleet supply across the broader market. With tonnage trapped inside the Middle East Gulf and bunker costs roughly doubling relative to the February average, demand concentrated on available tonnage outside the region, pushing spot rates higher. The prolonged closure had raised the prospect of an energy-driven recession weighing on global trade and dry bulk demand, so the ceasefire created a more promising outlook for economic activity. FFA markets jumped on the news, which likely fed through into spot rate gains as confidence returned.

One-year timecharter rates have been more stable, reflecting charterers’ reluctance to commit at elevated levels against an uncertain demand outlook, widening the gap between spot and period rates.

For smaller vessel classes, the picture is more subdued. Panamax, Supramax, and Handysize segments bear a greater share of the direct disruption, with trapped tonnage, cancelled fertiliser and grain liftings, and reduced Gulf port activity all weighing on utilisation.

Secondhand sales volumes fall as geopolitical uncertainty weighs on buyers

Bulker secondhand sales volumes held firm through the opening months of 2026 before retreating sharply as the Hormuz crisis took hold. January and February each recorded 94 and 95 sales respectively, broadly in line with the same period in 2025. March marked the turning point, with transactions falling to 60, roughly half the 122 recorded in March 2025. April has slowed further to just 15 sales to date, underlining the extent to which geopolitical uncertainty has weighed on buyer and seller appetite.

Notable recent sales include the Capesize Frontier Garland (181,500 DWT, 2011, Imabari) sold to Greek buyers for USD 36.5 mil, VV Value USD 34.8 mil. Additionally, the Supramax Valiant (55,600 DWT, 2009, Hyundai Vietnam) sold by Mercury Maritime for USD 13.4 mil, VV Value USD 13.6 mil.

Handy Bulkers have accounted for the largest share of year-to-date activity at 82 sales, followed by Panamax Bulkers at 57 and Supramax at 51. Despite the volume slowdown, values have remained firm across almost all sub-sectors and age categories. The strongest appreciation this year has been in the Supramax segment, where 60,000 DWT vessel values have risen 14.85% since January from USD 29.76 mil to USD 34.18 mil.

This outperformance likely reflects the segment’s versatility across commodity trades and relatively limited direct Gulf exposure compared to smaller classes. Firm values across the board suggest owners are taking a longer view, with the prospect of normalising trade flows and recovering dry bulk demand once the strait reopens — providing support to pricing despite the near-term uncertainty.

EXECUTIVE SUMMARY

Shipping Market Outlook: Q2 2026

Tankers, Bulkers, Containers, LPG