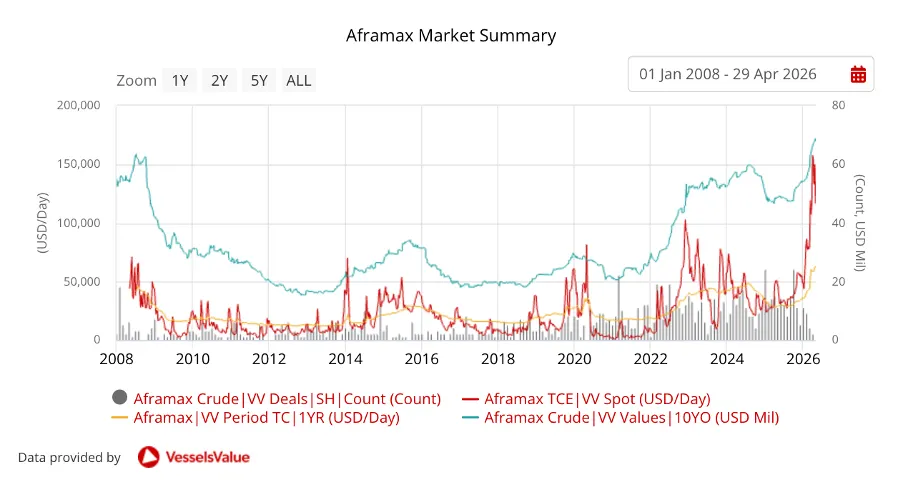

The Aframax market is in record territory. Values and earnings are at all-time highs, and the owner base shows little inclination to sell despite the extraordinary conditions.

Fixed age values for eight-year-old Aframaxes stand at USD 75.17 mil, the highest levels ever seen, compared to USD 53.08 this time last year, equating to an increase of c.42%. This increase in values has largely been driven by a surge in earnings.

One-year VV spot Aframax TCEs have been hovering around all-time highs, having reached a peak of 158,000 USD/day and at the time of writing is 116, 429 USD/day. The TC market also follows a similar pattern. One-year timecharter rates are also at an all-time high, currently sitting at 63,002 USD/day and are up by 119% from this time last year.

How the Strait of Hormuz disruption is reshaping tanker demand

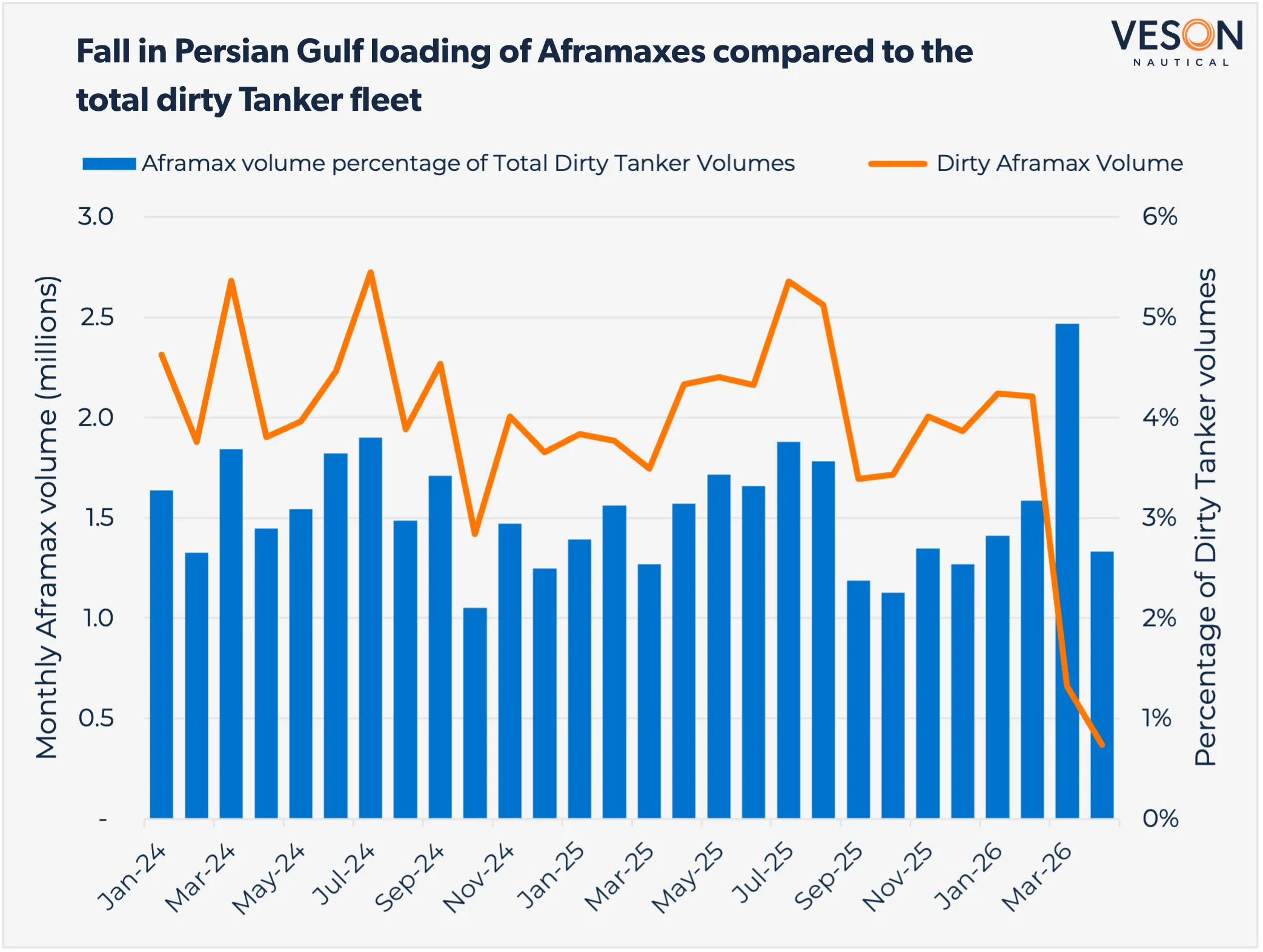

The primary driver behind this earnings surge has been the ongoing crisis in the Strait of Hormuz, through which Aframaxes moved an average of approximately 2 mil barrels of crude per month in 2025, a figure that has fallen sharply in early 2026 as the crisis has unfolded. US and Israeli military action against Iran, combined with a US naval blockade of Iranian exports, sent earnings sharply higher, curtailing cargo availability, prompting charterers to secure tonnage at elevated rates. Rerouting and increased voyage distances have added effective ton-mile demand without any corresponding increase in vessel supply, structurally tightening the available pool.

Compounding this, sanctions enforcement and the broader shadow fleet have concentrated mainstream chartering demand onto compliant, transparently owned tonnage, further supporting values for vessels with clean commercial records. Underpinning all of this is continued oil demand resilience; without sustained cargo volumes, earnings would not have held at these levels regardless of geopolitical disruption.

Aframax second hand and newbuilding prices reach near-parity

Second hand values have risen to the point where an eight-year-old Aframax of 110,000 DWT, currently valued at USD 74.15 mil, sits almost exactly at parity with a newbuilding of 115,000 DWT, valued at USD 74.24 mil.

At the same time, Aframax newbuilding appetite remains limited with just one vessel ordered so far in 2026, by Carlova Maritime, scheduled to be built at Hengli Shipbuilding and set for delivery in 2027, contracted for USD 75 mil, VV value USD 74.31 mil. This contrasts with 2025 levels where eight Aframax orders were placed over the same period.

Notable sales include the Aframax Pusaka Borneo (108,500 DWT, Nov 2018, Tsuneishi Zosen) which sold for USD 76.5 mil, VV value USD 77.69 mil, to Eurotankers. VesselsValue’s Fixed Age Analysis, which tracks the historical distribution of predicted market values for a standard vessel at each age across its lifespan, confirms that this transaction is not just a reflection of current market conditions.

On a like-for-like basis, the Pusaka Borneo is the most expensive Aframax ever sold. By holding vessel specification constant across the full historical range, the data shows that an eight-year-old Aframax has never previously transacted at these levels, making this a genuinely historic sale.

Other notable Aframax/ LR2 sales include the Southern Reverence (108,534 DWT, March 2018, Tsuneishi) that sold for USD 75 mil, VV value USD 76.36 mil, as well as the older scrubber fitted Torm Ganga (119,500 DWT, Nov 2010, Hyundai Samho HI) sold to Chinese buyers for USD 53.5 mil, VV value USD 56.48 mil.

Why Aframax sales volumes are falling despite record values

Despite record earnings and values, S&P volumes have fallen significantly, and the volume of Aframax sales is roughly half what it was for the same period last year. So far in 2026, there have been 25 sales reported, compared to 62 in the same period in 2025. The average age of vessels sold this year is 17, which suggest that those transacting may be offloading older tonnage rather than prime assets, whilst buyers might be taking advantage of lower price points in these sectors in order to take advantage of high earnings, a trend that has emerged over the last few years with many vessels entering into the ‘dark fleet’.

On the whole, owners are not cashing out despite the high values which could indicate that they believe there could be further upside. Recent buyers ranged from a variety of countries with China being the most dominant, accounting for c.16% of purchases.

EXECUTIVE SUMMARY

Shipping Market Outlook: Q2 2026

Tankers, Bulkers, Containers, LPG