Offshore support vessels(OSV) values have risen more than tenfold from their 2019 trough, reaching levels that would have seemed implausible five years ago. What makes this cycle particularly compelling, however, is the near-empty PSV and AHTS orderbook at c.4% combined — a structural constraint that points to a sustained upside and, potentially, a prolonged golden era for asset values.

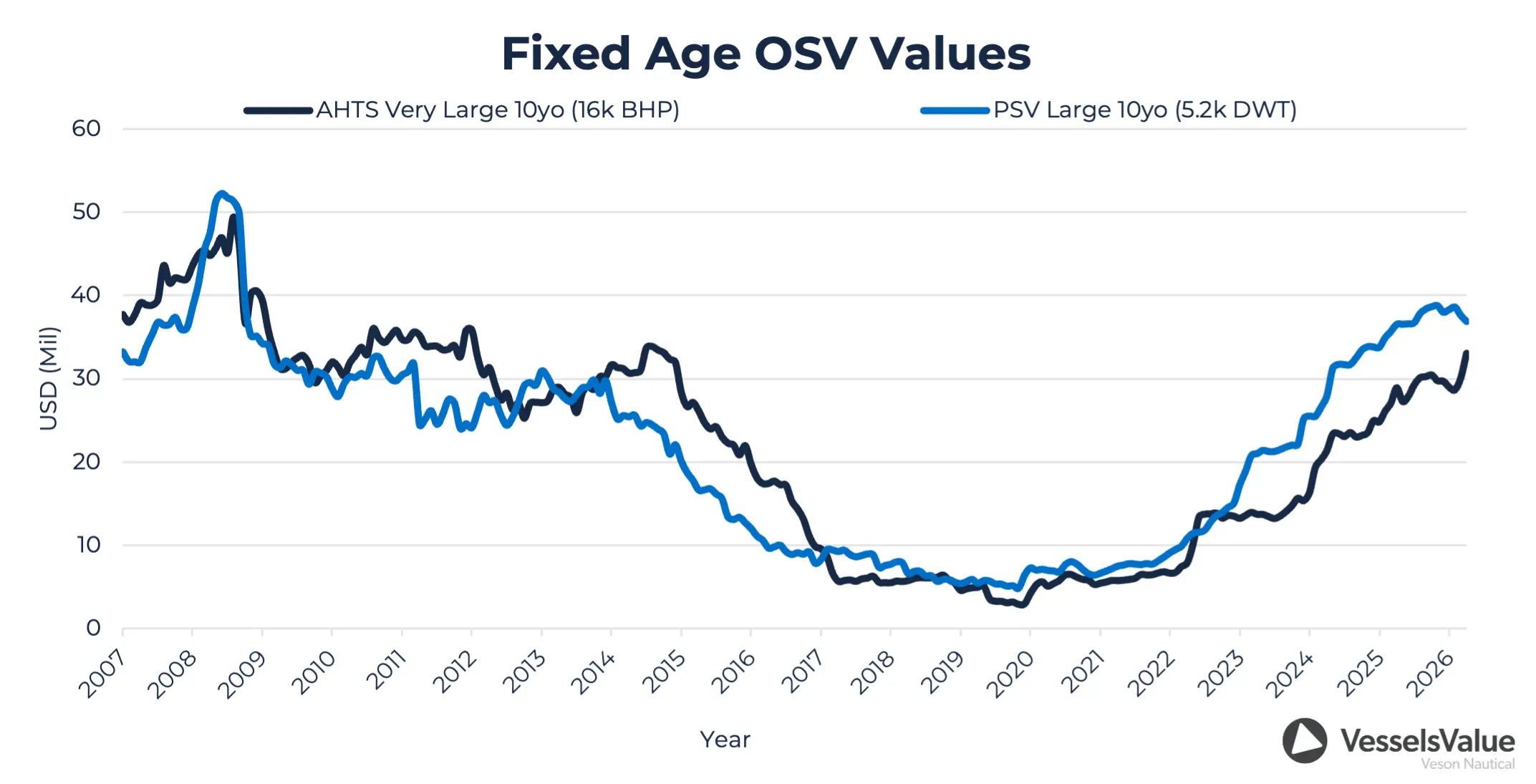

In the summer of 2008, with oil above $100 a barrel and the offshore sector ordering at its most aggressive in a generation, OSV values reached their highest recorded levels. A 10YO AHTS Very Large was worth close to VV USD 50 mil, and a PSV Large was fetching similar numbers. Vessels of all ages were commanding strong prices, with buyers unable to afford to be selective given how tight supply had become across the fleet.

When oil collapsed later that year, values followed sharply. They found a floor through the early 2010s as oil recovered and E&P spending remained healthy, but a heavy supply overhang prevented any meaningful upside. When oil fell again in 2014, the fleet was already oversupplied and the two pressures together sent values into freefall. By late 2019 both vessel types had lost more than c.90% of their peak value.

Previous Market Recovery

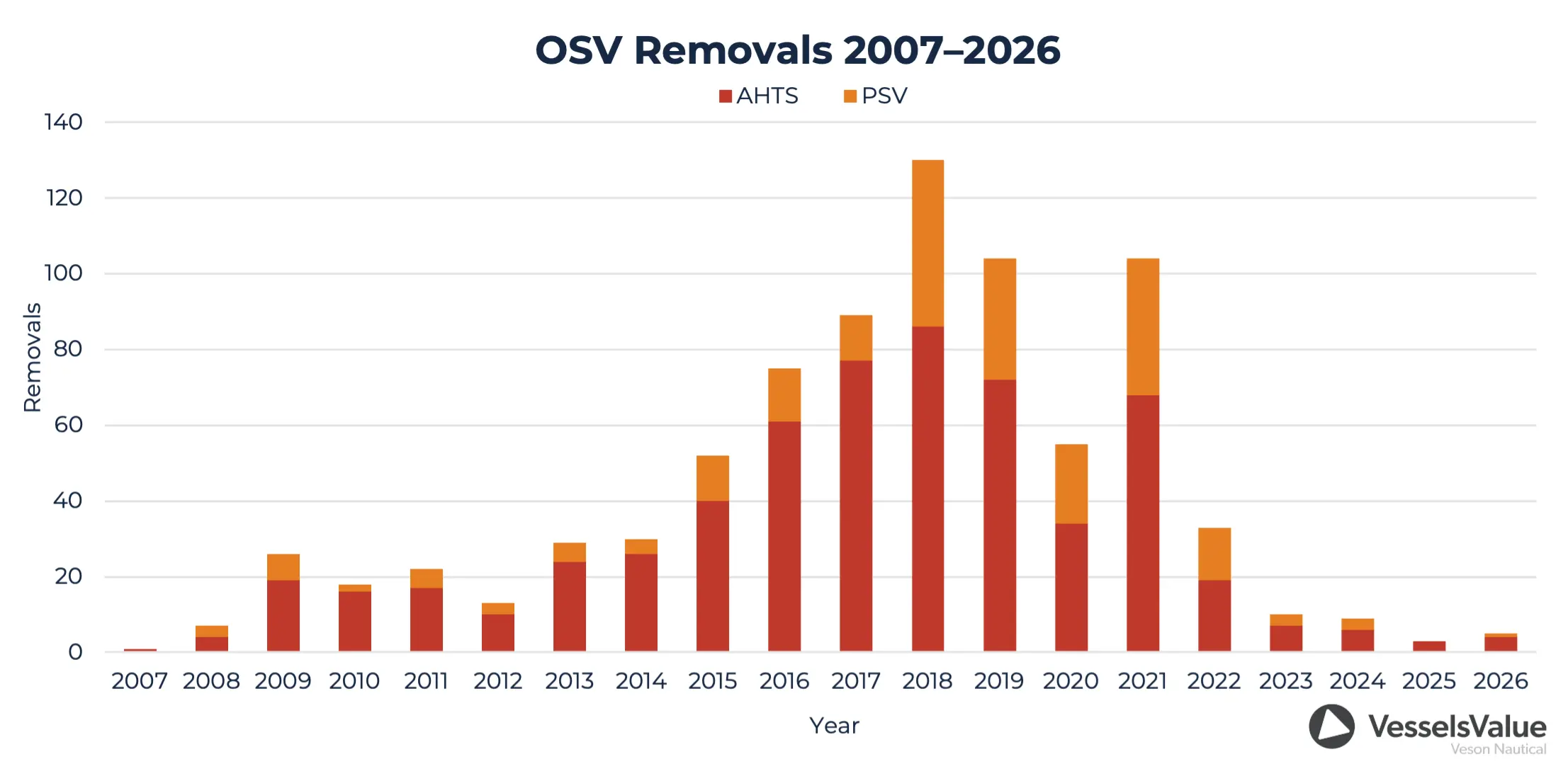

Scrapping peaked at 130 vessels in 2018, as operators cleared older tonnage at the bottom of the market. Since then, the trend has reversed entirely. Only three vessels have been removed so far in 2026, and with newbuild costs running well above what the current market can justify, vessels that might previously have been retired at 20 years of age are being dry-docked and kept working. The fleet is older than it has ever been, with the average PSV and AHTS now more than 20-years-old. Rather than replacing tonnage, owners are squeezing more life out of what they have, and for now the market is rewarding them for it.

Today’s Orderbook

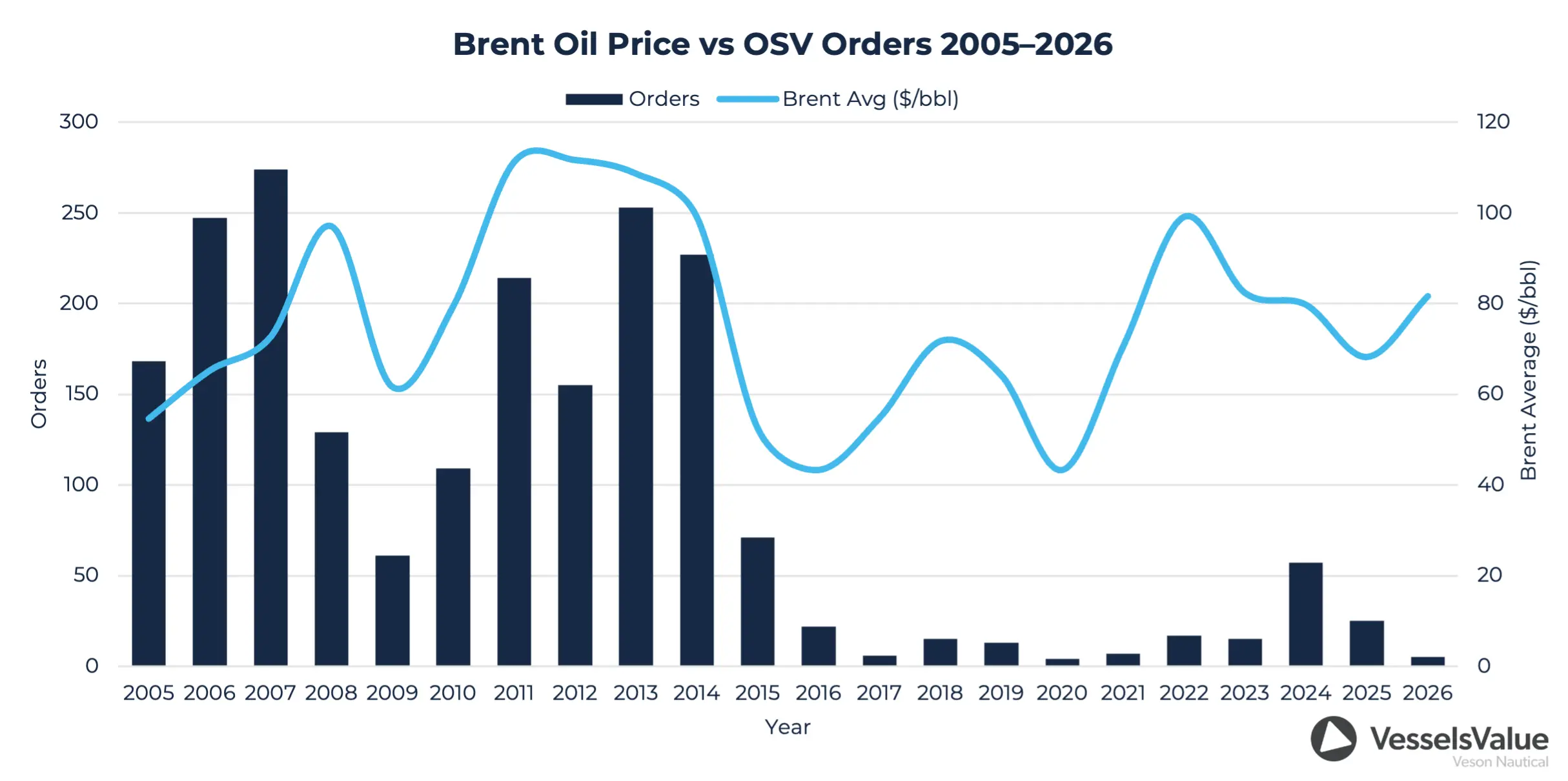

The ordering booms of the past two decades were oil price events. As Brent climbed through the mid-2000s, owners ordered aggressively, and by early 2008 there were over 900 PSVs and AHTS on order, representing more than a third of the live fleet. The financial crisis broke the first peak but not the ordering habit, and owners continued placing vessels well into the recovery. By 2017 the fleet had swelled to nearly 5,000 vessels. The sector had built itself into a structural oversupply that took the better part of a decade to work through.

As of today, four years into a strong recovery and with Brent above USD 100/barrel, the combined PSV and AHTS orderbook stands at just 4% of the live fleet. In the previous two market cycles, the orderbook sat at 34% and 15% at comparable points. Owners who lived through two rounds of ordering into rising values and then watching those same values collapse have drawn a different conclusion this time: run the existing fleet harder and longer, rather than commission new tonnage. Scrapping has virtually stopped, older vessels are being maintained and redeployed, and the fleet has strong utilization levels.

The 179 vessels currently on order are largely comprised of Chinese-built mid-range tonnage and project specific PSV builds for Petrobras in Brazil. There is currently no AHTS on order globally that is above 12k BHP.

What This Means for the Market

The current orderbook is dominated by mid-range PSVs and small AHTS. The absence of larger AHTS and PSV newbuilds remains, and the deliveries that are coming will not change the supply picture at the top end of the fleet. With an ageing global fleet, rising E&P spending and operators continuing to defer replacement decisions in favour of life extension, the market looks short supplied into the medium term, which is bullish for PSV and AHTS asset values.

But the more interesting question is what the supply vacuum means for those considering new tonnage. High-spec AHTS values and dayrates are at multi-year highs, E&P spending is accelerating, and Brazil, Australia and the North Sea are all competing for a shrinking pool of capable tonnage. The owners who lived through the last downturn will not repeat the mistakes that ended it, and that collective restraint is precisely what makes the case for ordering today. With yard lead times of three to four years, a newbuild ordered now would deliver into the tightest market in a generation, and modern high-spec tonnage carries the flexibility to pivot toward offshore wind and subsea work as those markets mature beyond the mid-2030s.

The economics that once made ordering irrational have quietly reversed. The last cycle punished those who ordered too much. This one may punish those who order too little.