The global shipping market is navigating Q2 2026 under the ongoing weight of an unprecedented geopolitical shock. The de facto closure of the Strait of Hormuz, now entering its third month, has fundamentally reshaped trade flows and earnings dynamics across all sectors. With no credible resolution in sight and the US military reported to be blocking vessels exiting the Strait, market uncertainty shows no signs of easing.

Tanker earnings reaching record levels in Q1 2026, with Aframax values hitting all-time highs in May. Bulkers have shown surprising resilience and container markets remain broadly stable, while the LPG market has experienced notable disruption of trade flows.

Across all segments, how the conflict evolves from here will be the defining variable for the remainder of 2026. The duration of the Hormuz closure, the pace of any oil supply recovery, and how markets adapt to fundamentally altered trade routes will have direct consequences for utilization, earnings, and asset values across the fleet.

Download the full Q2 2026 Shipping Market Outlook Executive Summary here and read the sector-by-sector preview below:

Tankers

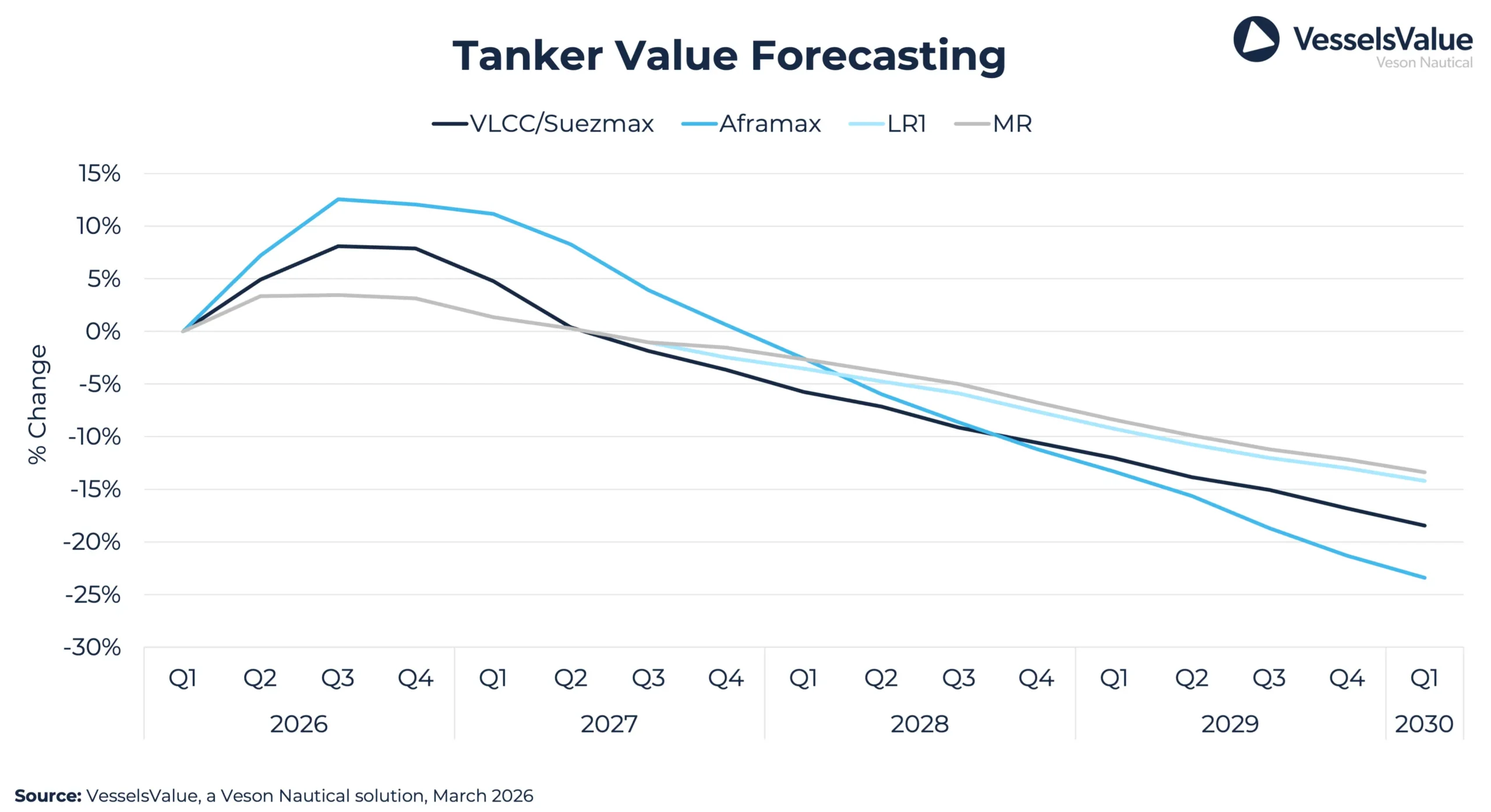

- VLCC earnings averaged around $175,000/day in Q1 2026, record quarterly levels, as the Strait of Hormuz closure removed roughly 25% of global seaborne oil trade from the market.

- The two-week US-Iran ceasefire announced in early April is now on the verge of collapse, adding a significant new layer of uncertainty for market participants.

- The Tanker orderbook now represents 20% of the total fleet, with effective fleet growth negative in 2026 before outpacing demand growth from 2027 through 2029

Aframax values and earnings are also in record territory. Read Senior Content Analyst Rebecca Galanopolous’ latest analysis here.

Bulkers

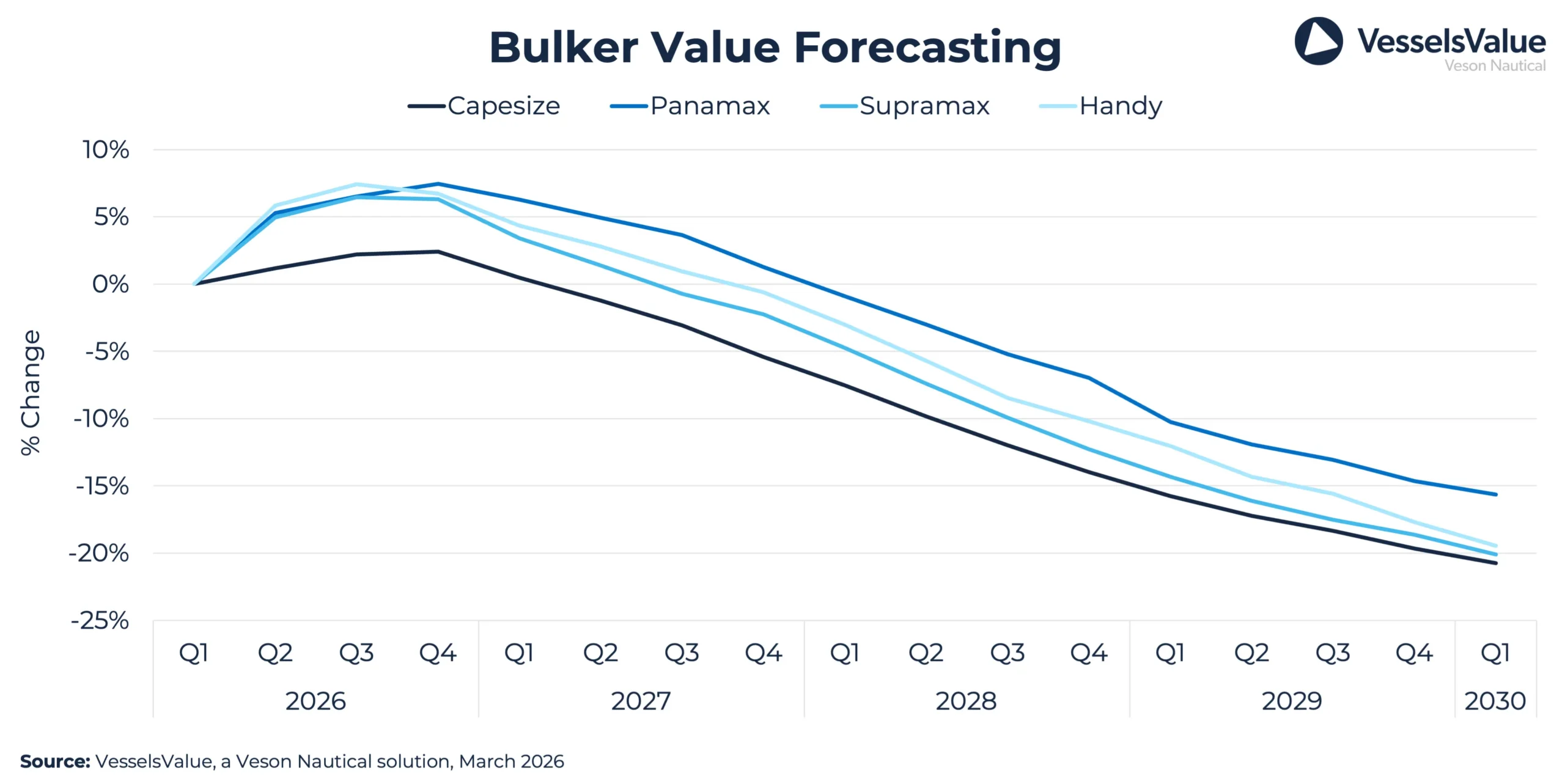

- The Bulker market defied typical seasonal weakness in Q1 2026, with Capesizes averaging around $23,000/day, up approximately 75% year-on-year, driven by strong Chinese import demand.

- The gradual ramp-up of Guinea’s Simandou iron ore mine, with its substantially longer sailing distances to China, provides an important structural ton-mile offset over the outlook period.

- Demand growth of approximately 2.7% per year over 2026-2029 is projected to be outpaced by supply growth of 3.3% per year as ordered vessels enter service in 2027 and 2028.

Curious how the potential Guinean export cap could reshape Capesize demand? Read Senior Maritime Analyst Mikkel Nordberg’s latest analysis here.

Containers

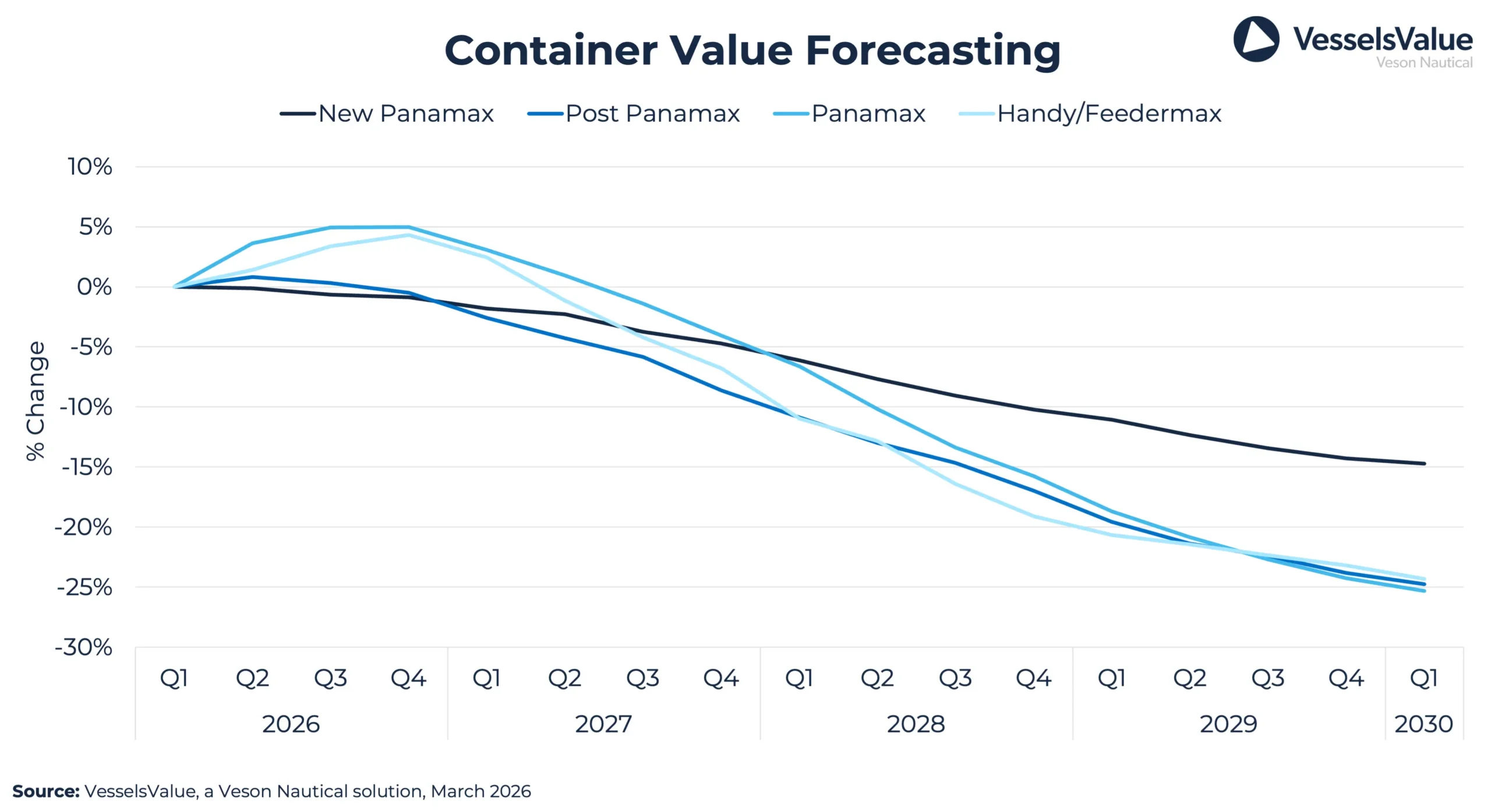

- Container earnings were broadly stable in Q1 2026, with Red Sea diversions and tight vessel availability providing support even as Asia-North America volumes fell 7.4% in January 2026 on tariff headwinds.

- TEU-mile demand growth is forecast at 1.4% in 2026, constrained by weaker volumes on Asia-Europe and Asia-North America routes, before recovering to average growth of approximately 4% per year from 2027 to 2029.

- The orderbook stands at 36.6% of the existing fleet, with freight rates forecast to decline 25.2% on average over the forecast period.

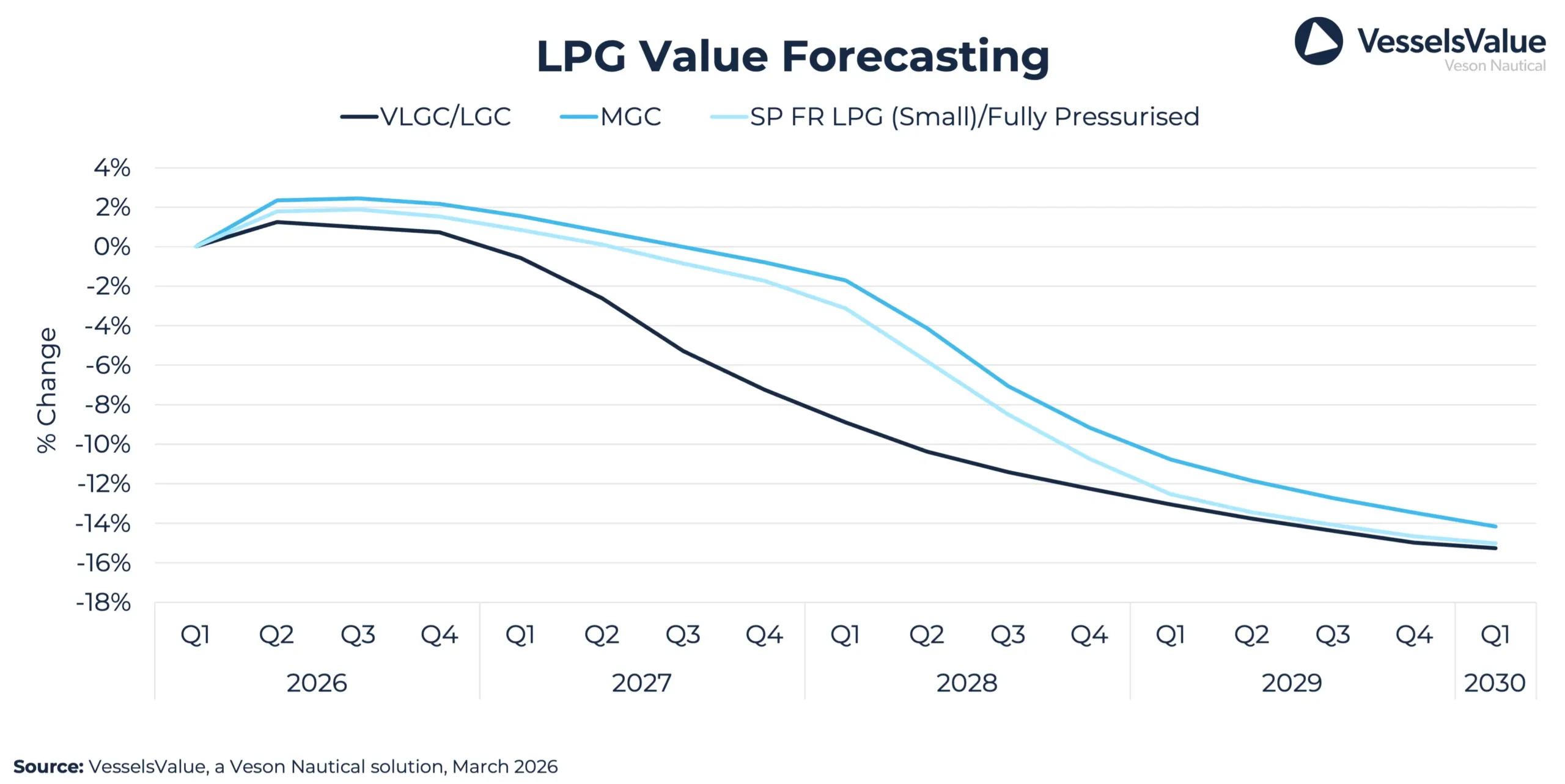

Gas

- The Strait of Hormuz closure removed approximately 30% of global LPG supply from the market, with VLGC earnings averaging around $75,000/day in Q1 2026, up 56% year-on-year.

- Approximately 25% of global ammonia exports originate from the Middle East, and the ongoing conflict is expected to delay near-term seaborne ammonia trade growth.

- US LPG exports are projected to grow 7.1% in 2026, though significant fleet deliveries are expected to weigh on market balance from 2027.

Download the full Q2 2026 Executive Summary to see how the major shipping markets could continue to unfold.

All information provided is for informational purposes only. To the extent that any provided information is based on Veson Data, Veson excludes to the extent permitted by law all implied warranties relating to fitness for a particular purpose, including any implied warranty that Veson Data is accurate, complete, or error free. Veson Data are collated and processed by and on behalf of Veson in accordance with methodologies and assumptions published and updated by Veson from time to time which do not take into account particular circumstances applicable to individuals and therefore; (i) are made available on an ‘as is’ basis; (ii) are not intended as a substitute for formal valuations; (iii) should not be used solely as trading, investment, or other advice; and (iv) are not intended as a substitute for professional judgement. To the extent permitted by applicable law, Veson shall have no liability to party for any errors or omissions in the content of the information provided.